Home / Life Insurance / Articles / How to Cancel a Life Insurance Policy?

How to Cancel a Life Insurance Policy?

Shreya SahuMay 13, 2026

Share Post

To cancel a life insurance policy, you may need to contact the insurer through customer care, email, or by visiting a branch. You may be asked to submit a written cancellation request, along with policy documents and proof of identity. As a policyholder, you have the option to go through the insurance policy and opt out of it within a 15-day free look period (30 days in the case of electronic policies) after receipt of the policy, in case you are not satisfied with the terms and conditions of the policy, by mentioning the reasons for cancellation.

Contents

- What Are the Ways to Cancel a Life Insurance Policy?

- Process to Cancel Your Life Insurance Policy

- What Happens When You Cancel a Life Insurance Policy?

- How Much Money Will You Get If You Cancel Life Insurance?

- Charges and Deductions on Cancellation of Life Insurance

- Key Things to Consider Before Cancelling a Life Insurance Policy

- Alternatives to Cancelling Your Policy

- Final Thoughts

- Frequently Asked Questions

What Are the Ways to Cancel a Life Insurance Policy?

Some available options to cancel a life insurance policy include:

Free Look Cancellation: The policyholder can cancel the policy within 15 to 30 days of receiving the documents. Moreover, the policyholder may obtain a refund of the premium paid, subject to the policy terms and applicable deductions.

Talk to Your Policy Holder: The most suitable way to cancel a life insurance policy is to first talk to your policy holder. Informing the policyholder about the cancellation can make the process easier.

Surrendering the Policy: For policies such as Whole Life Insurance and ULIP, the policyholder can cancel the policy. In this case, the policyholder may receive the surrender value, depending on the policy terms and duration.

Stop Payment (Lapse): If premiums are not paid, the policy lapses and will be cancelled by the insurer. Additionally, you will lose all accumulated value.

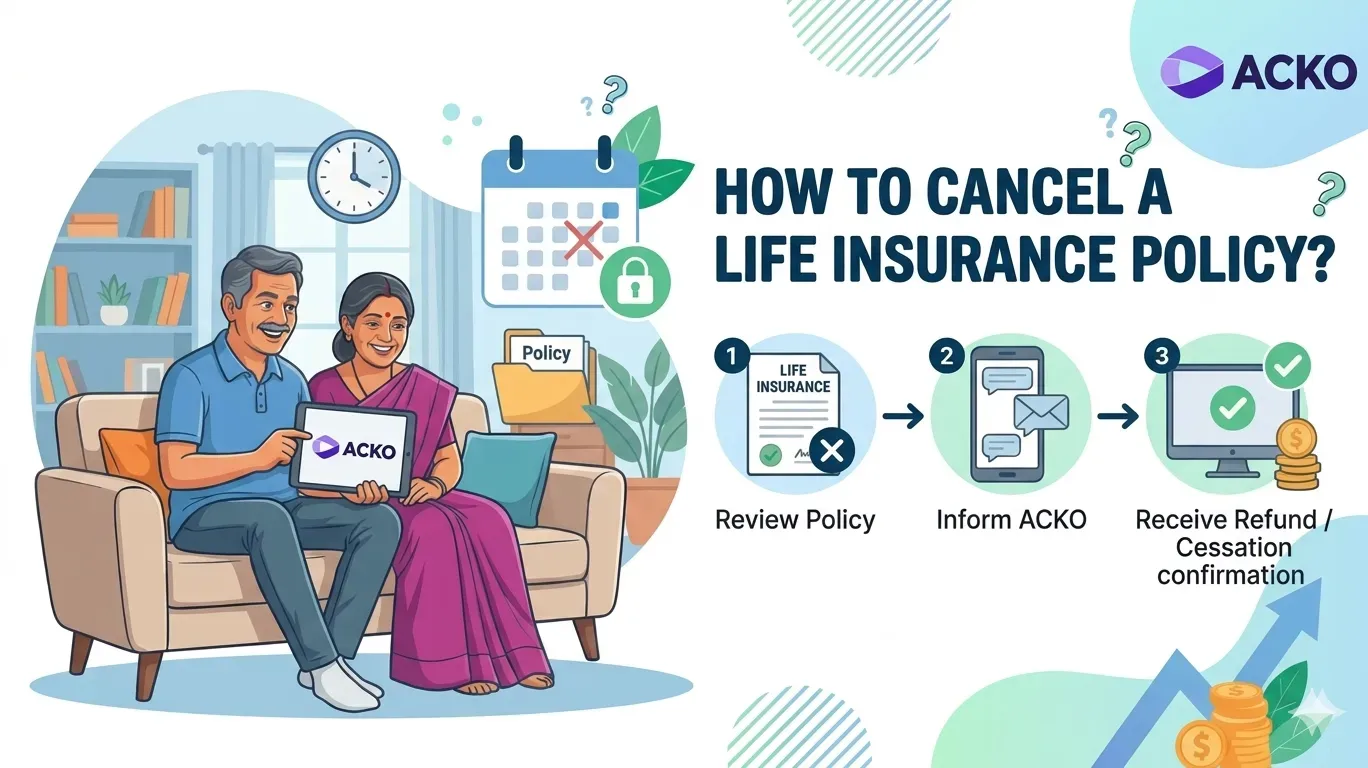

Process to Cancel Your Life Insurance Policy

Follow these steps if you are wondering how to cancel a life insurance policy online.

Step 1: First, visit the official website or app of your insurance provider.

Step 2: Log in to your account

Step 3: Look for sections such as ‘policy services’ or ‘policy management’ to find options for cancellations.

Step 4: Download the cancellation form and carefully fill in the details, including the reason for your cancellation.

Step 5: Upload the documents, including your PAN, Aadhar, ID Proof, cancelled cheque and original policy document.

Step 6: Once submitted, you will receive a reference number to track your submission.

What Happens When You Cancel a Life Insurance Policy?

Cancelling a life insurance plan immediately terminates your coverage, resulting in a loss of the death benefit. Here is the detailed explanation of what happens when you cancel a life insurance policy.

Loss of Coverage: Coverage stops immediately upon cancellation. This leaves beneficiaries without a death benefit payout.

Reapplication Difficulty: If you choose to buy a new policy later, you might have to pay higher premiums due to increased age or worsening health.

No/Partial Refund: Usually, if you cancel a life insurance policy, you might not receive any premium.

Outstanding Loans: If you have taken a loan against the policy, cancelling it may require you to pay the outstanding balance immediately.

ULIP Lock-In: ULIPS have a 5-year lock-in period. If surrendered early, the money is moved to a ‘discontinued policy fund’ and paid only after the 5-year period ends.

How Much Money Will You Get If You Cancel Life Insurance?

The amount of money you might receive after cancelling your life insurance plan depends on certain factors. It includes the plan type, the plan duration, and the surrender value rules. It has also been noted that the payout amount may be lower during the initial period, increasing over the course of the plan.

So, here is a discussion of the payouts at various stages:

Within the Free-Look Period (15–30 days): You may get a refund of the premium paid after deducting some nominal administrative or medical expenses.

Before Completing 3 Years: You may not get a surrender value, especially in traditional policies. The payout may be zero or negligible in such cases.

After 3+ Years of Premium Payments: You may become eligible to receive a Guaranteed Surrender Value (GSV). The GSV is normally 30% of the total premium paid, excluding the first year’s premium and the cost of any rider premium paid.

Later Years (Higher Policy Duration): You may also receive Special Surrender Value (SSV), which is generally higher than GSV. The SSV is normally determined according to the insurer’s own formula.

Term Insurance Policies: These policies normally do not build up cash value. Hence, the payout may not be applicable in such cases.

Disclaimer: At ACKO, if applicable, the surrender value may be paid as a lump sum amount at the time of policy cancellation, subject to the policy terms and conditions.

Charges and Deductions on Cancellation of Life Insurance

Depending on the life policy type, the following charges may apply:

Term | Description |

|---|---|

Surrender charges | A fee deducted by the insurer when you cancel a life policy before it matures. |

Discontinuance charges (ULIPs) | Charges may apply if a ULIP policy is discontinued during the lock-in period. |

Administrative charges | Fees the insurer collects for processing and managing the policy. |

Stamp duty deductions (during free look) | The government stamp duty amount is deducted if a policy is cancelled during the free-look period. |

Medical examination cost deductions | Expenses for medical tests may be deducted if you cancel the policy after the tests are conducted. |

Note: These charges may reduce the final amount you receive. Always request a surrender value estimate before cancelling.

Key Things to Consider Before Cancelling a Life Insurance Policy

Before cancelling a life insurance policy, it is helpful to review the financial implications and explore possible alternatives.

Timing

Timing is crucial when cancelling a life insurance policy. If you act within the free-look period (15–30 days after purchase), you can cancel without any penalty. However, cancelling much later can lead to financial loss. For example, surrendering a policy after 20 years may return some money, but you could lose valuable long-term benefits and coverage.

Tax Implications

If you claimed tax benefits on premiums under Section 80C of the Income Tax Act 1961 and cancelled the policy before maturity, those benefits may be reversed. Early withdrawal from ULIPs before the lock-in period may also attract taxes.

Risk of Increased Premiums

Cancelling a life insurance policy at present may have an impact on future policies. If you apply again later, your premium may be higher due to age and health conditions.

Alternatives to Cancelling Your Policy

Instead of cancelling your life insurance policy, you may consider the following alternatives:

Reducing the Sum Assured: You may consider reducing the sum assured, as some insurers allow such adjustments.

Converting to Paid-Up Policy: Consider converting your policy to a paid-up policy. You may stop paying, but your coverage will continue at a lower amount.

Revival of Policy: If your policy has lapsed, it may be possible to revive it within a specified period, subject to the insurer’s terms.

Partial Withdrawal (for ULIPs): After the lock-in period, partial withdrawals may be allowed.

Reviewing Financial Plan: You may consider restructuring and reviewing your finances instead of surrendering a long-term plan.

Exploring these options may help you avoid financial loss.

Final Thoughts

The decision to cancel a life insurance policy mostly depends on your immediate and future financial needs. Before cancelling your policy, it is important to understand its benefits, charges, and alternatives. Overall, understanding the procedure of cancelling a policy will help you make a better decision.

Frequently Asked Questions

Below are some of the frequently asked questions on How to Cancel a Life Insurance Policy?

Can I cancel my life insurance policy at any time?

Yes, you may cancel your life insurance policy at any time. However, the outcome and the benefits may depend on the type of policy you have.

Will I get my money back if I cancel my life insurance policy?

If you cancel the life insurance policy during the 15-30 day free look period, you may get a near full refund. After this policy, with savings components such as endowments or ULIPs, offer a surrender value.

How much will I receive if I surrender my life insurance policy?

The amount depends on the policy type, duration, premiums paid and applicable surrender charges deducted by the insurer.

How long does it take for cancellations in a life insurance policy?

It may take a few days to a few weeks, depending on the insurer’s process and the required documents.

What is the free look period in life insurance?

It is a time window typically 15-30 days. This period allows the policyholder to review and cancel the policy if they want.

Does cancelling a life insurance policy affect my credit score?

No, it does not affect your credit scores. It is because it is not linked with loans or credits.

Explore Life Insurance Product

Was this article helpful?

Recent

Articles

Do ADAS Features Reduce Car Insurance Premiums in India?

Nikhila PS Jun 25, 2026

How Do BS6 Bikes Affect Bike Insurance Premiums and Coverage?

Nikhila PS Jun 25, 2026

Does Health Insurance Cover Recurrent Depressive Disorder?

Neviya Laishram Jun 25, 2026

Top 15 Car Companies in India in 2026

Nikhila PS Jun 25, 2026

Does Two-Wheeler Insurance Cover Dents and Paint Damage?

Nikhila PS Jun 24, 2026

All Articles

Want to post any comments?

ACKO Term Life insurance reimagined

ARN:L0072|*T&Cs Apply

Check life insurance

#36/5, Hustlehub One East, Somasandrapalya 27th Main Rd, Sector 2, HSR Layout, Bengaluru, Karnataka 560102