Home / Health Insurance / Articles / How Does Health Insurance Work in India

How Does Health Insurance Work in India

Neviya LaishramMay 26, 2026

Share Post

In India, health insurance helps policyholders cover their medical costs in return for paying a premium to the insurer. From cashless treatment at network hospitals to reimbursement claims for surgery, dengue admission, maternity services, and day care services, understanding how health insurance works could help ease financial burden during emergencies.

In this guide, you’ll learn how health insurance works, how claims are processed, the role of deductibles, and the key difference between mediclaim and health insurance plans.

Contents

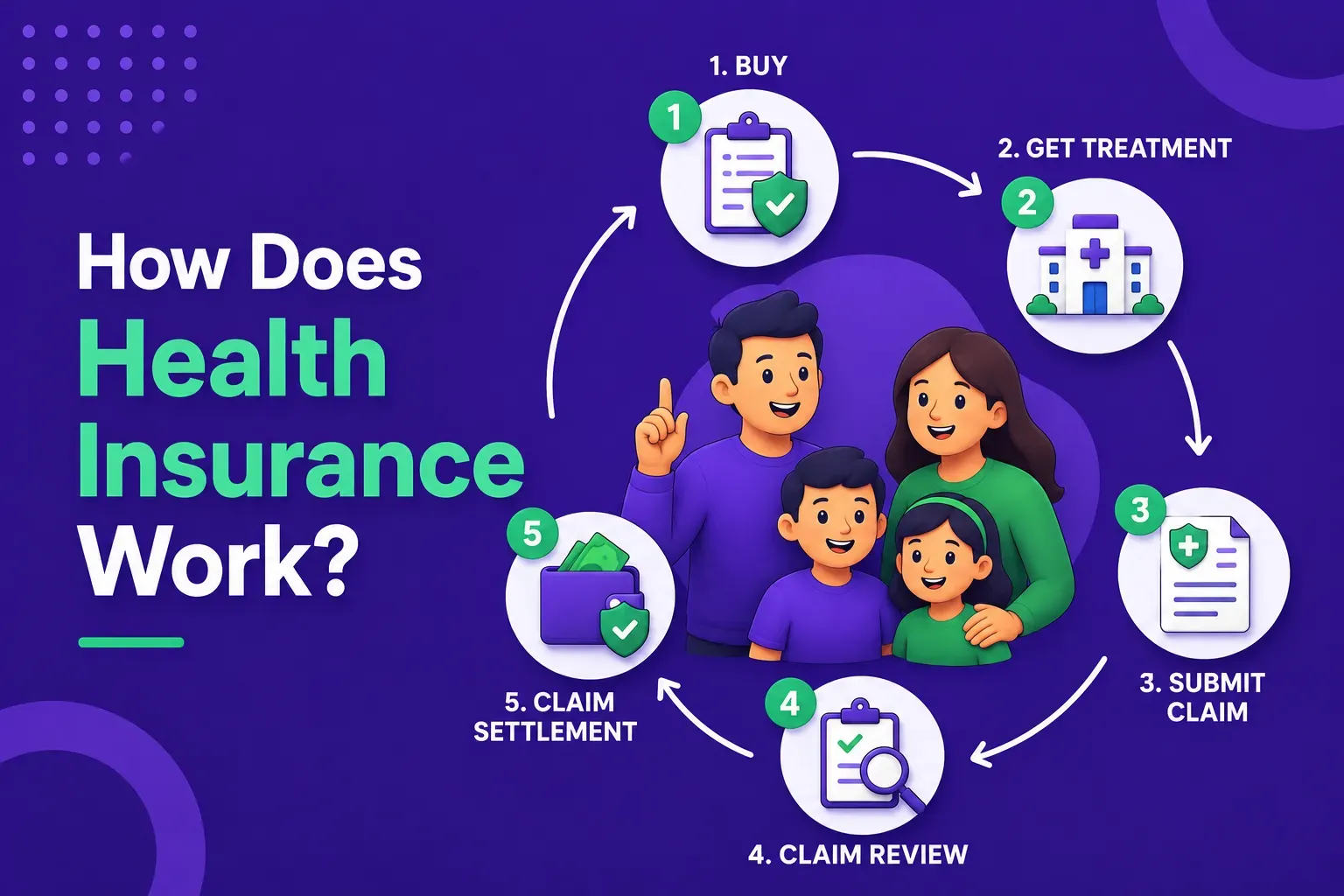

How Does Health Insurance Work?

Health insurance works like this: you pay a small, fixed amount every year (the premium), and in return, your insurer takes care of your medical bills when you actually need them.

Let's understand how health insurance works with a simple example.

Priya, who is 30 years old, is a software engineer from Bengaluru. She bought a health insurance plan with a sum insured of ₹10 lakh and pays just ₹8,000 as her yearly premium, which is less than ₹700 a month.

One year later, she was diagnosed with appendicitis and needed emergency surgery. The total hospital bill came to ₹1.2 lakh. That's a big amount to pay all at once.

But here's where her health insurance came in. Since her hospital was in her insurer's network, she didn't have to pay the bill herself. Her insurance company settled it directly with the hospital. All Priya had to do was show her insurance card at the time of admission and sign a few forms. Her savings remained untouched.

How Do Health Insurance Claims Work?

A health insurance claim is an official request you submit to your insurance company to cover the cost of your medical bills. There are usually two ways this occurs:

Cashless Claim: The insurer pays the hospital directly.

Reimbursement Claims: You pay the bill yourself, and then you get reimbursed by the insurer.

H3 Cashless Treatment at Network Hospitals

Cashless health insurance is one of the most convenient ways to receive medical treatment. You can get treated at network hospitals without paying the full hospital bill during admission or discharge. Here’s how the process usually works:

Visit a network hospital and share your health insurance card or policy details.

The hospital sends a pre-authorisation request to the insurance company or TPA.

Once the claim is approved, the insurer settles the eligible hospital expenses directly with the hospital.

You only need to pay for uncovered expenses such as consumables, registration charges, or non-medical items.

Reimbursement Claims Process

If you get treated at a non-network hospital, you will need to pay the hospital bill yourself at the time of discharge. You can later submit a health insurance claim form along with hospital bills, discharge summaries, prescriptions, and other required documents to your insurer for reimbursement of eligible expenses.

Cashless vs Reimbursement Claims

Mediclaim Vs Health Insurance: How Do They Differ?

Many people use these terms interchangeably, but there is a slight difference between mediclaim and health insurance:

If you already have health insurance, check if your health policy covers everything you need.

Conclusion

Understanding how health insurance works can help you manage medical emergencies with less financial stress. When selecting a plan, consider factors such as network hospitals, claim settlement efficiency, and a smooth claims process to ensure better financial protection and peace of mind.

FAQs

Below are some frequently asked questions about How Does Health Insurance Work in India

How can I check the status of my health insurance claim?

Instantly check your health insurance claim status on the ACKO app.

What documents are needed for reimbursement in India?

You generally need a filled claim form, original hospital bills, discharge summary, prescriptions, diagnostic reports, and bank details. Insurers may ask for additional documents based on the claim.

Is cashless treatment available in all Indian hospitals?

No, cashless treatment is mainly available at network hospitals tied up with your insurer or TPA. At non-network hospitals, you usually need to pay first and later file a reimbursement claim.

Can we claim health insurance from two companies?

Yes, you can claim health insurance from multiple insurers. If one policy does not fully cover your medical bill, you can use a second policy to claim the remaining eligible amount.

What is a health insurance deductible?

A health insurance deductible is the amount you pay from your own pocket before the insurer starts covering eligible medical expenses. Plans with higher deductibles often come with lower premiums.

How does cashless health insurance work?

In cashless health insurance, the insurer directly settles eligible hospital bills with a network hospital after the claim is approved. The policyholder only pays for uncovered expenses, if any.

Was this article helpful?

Recent

Articles

Do ADAS Features Reduce Car Insurance Premiums in India?

Nikhila PS Jun 25, 2026

How Do BS6 Bikes Affect Bike Insurance Premiums and Coverage?

Nikhila PS Jun 25, 2026

Does Health Insurance Cover Recurrent Depressive Disorder?

Neviya Laishram Jun 25, 2026

Top 15 Car Companies in India in 2026

Nikhila PS Jun 25, 2026

Does Two-Wheeler Insurance Cover Dents and Paint Damage?

Nikhila PS Jun 24, 2026

All Articles

Want to post any comments?

Discover our diverse range of Health Insurance Plans tailored to meet your specific requirements🏥

✅ 100% Room Rent Covered* ✅ Zero deductions at claims ✅ 7100+ Cashless Hospitals

Check health insurance

#36/5, Hustlehub One East, Somasandrapalya 27th Main Rd, Sector 2, HSR Layout, Bengaluru, Karnataka 560102