Home / Life Insurance / Articles / Limited Pay vs Regular Pay in Term Insurance: Key Differences Explained

Limited Pay vs Regular Pay in Term Insurance: Key Differences Explained

Shreya SahuMay 20, 2026

Share Post

Term insurance is one of the simplest ways to ensure financial security for your family’s future. When buying a term insurance plan, one important decision is how you will pay the premiums. Your choice may depend on your income pattern and long-term financial planning.

This blog explains the limited pay vs regular pay in term insurance and what you may consider before choosing between them.

Contents

- What is Limited Pay in Term Insurance?

- What is Regular Pay in Term Insurance?

- Difference between Limited Pay and Regular Pay in Term Insurance

- Pros and Cons of Limited Pay in Term Insurance

- Pros and Cons of Regular Pay in Term Insurance

- Factors to Consider Before Choosing a Premium Payment Option

- Final Thoughts

- Frequently Asked Questions

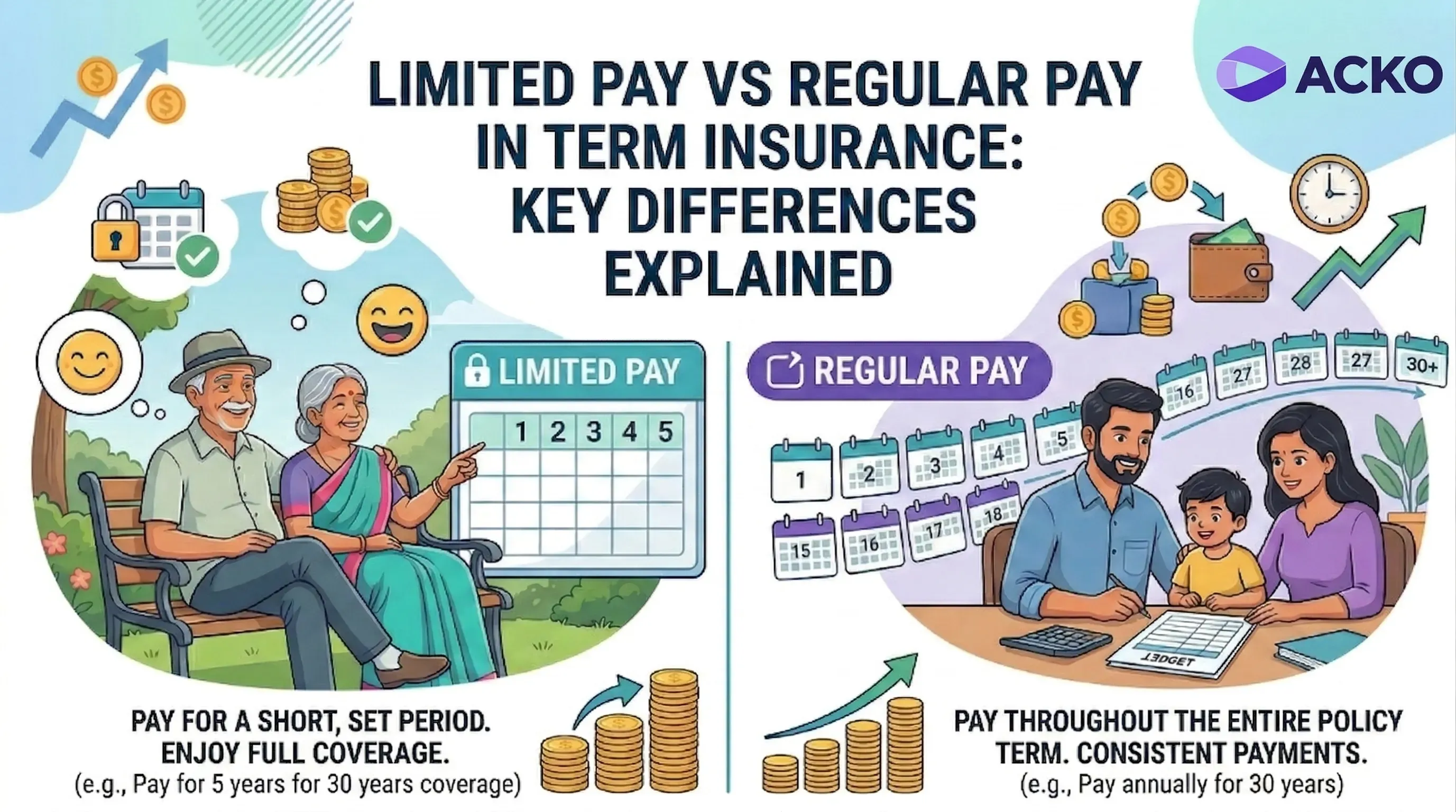

What is Limited Pay in Term Insurance?

Limited pay term insurance is a type of life insurance plan where you can make premium payments for a limited number of years, while you can enjoy the coverage of the insurance policy for the entire term without any further premium payments.

Let’s understand this with a simple example.

You purchase a term insurance policy for 30 years. If you choose limited pay, you may pay premiums only for 10–15 years. However, the policy continues for the full 30-year term. This option may suit individuals who prefer to complete premium payments earlier.

What is Regular Pay in Term Insurance?

Regular pay in term insurance means that you continue to pay premiums as long as the policy is in force. You do not stop making payments before time; instead, you make a fixed payment at regular intervals, such as monthly or quarterly, until the policy ends.

For instance:

If you choose a 30-year term policy, you would pay a premium every year for 30 years to renew the policy. This is a good option for those who prefer to make a low payment at regular intervals rather than a high payment at a particular time.

Difference between Limited Pay and Regular Pay in Term Insurance

The table below outlines the key differences between limited pay and regular pay term insurance:

Features | Limited Pay | Regular Pay |

|---|---|---|

Premium Duration | Premiums are paid for a shorter, fixed period (e.g., 10–15 years in a 30-year policy). | Premiums are paid throughout the entire policy term. |

Premium Amount | Usually higher per instalment | Usually lower per instalment |

Tax Benefits | Tax deductions may be available for premiums paid under applicable tax laws | Tax deductions may be available each year while premiums are paid, subject to tax rules |

Suitable For | Individuals who prefer completing premium payments earlier | Individuals who prefer spreading payments over a longer period |

Pros and Cons of Limited Pay in Term Insurance

The pros of Limited Pay in term insurance include:

You can complete your financial obligations early and can reduce long-term financial commitments.

The coverage generally continues after the premium payment period ends, subject to policy terms.

It may help you avoid making premium payments during retirement years.

Apart from the pros, limited pay in term insurance may have some cons (disadvantages), and these include:

The premium cost is higher than that of the regular payments.

It needs a stronger financial capacity during the early years.

Missing premium payments may affect policy continuity, depending on the policy's terms.

Pros and Cons of Regular Pay in Term Insurance

Regular pay plans are commonly chosen because premiums are spread across the policy term. However, it also comes with certain drawbacks that you might need to consider.

The pros of regular pay in term insurance include:

It has lower premium instalments due to its longer payment options.

This may be easier for some individuals to manage.

It may suit individuals with long-term income stability.

It has a lower immediate financial burden.

The drawbacks of regular pay in term insurance are:

Premium payments continue for the entire policy term that you have chosen.

Since it requires a long-term financial commitment, it may become difficult for some individuals.

The total premium paid over time may be higher than limited pay options in some cases.

Read More: How Much Life Cover Do You Really Need?

Factors to Consider Before Choosing a Premium Payment Option

To choose the right premium payment option, you might need to consider a few factors, such as your income stability and your financial planning. To know what factors you must consider before choosing a premium payment option, read the pointers below:

Income stability: First, assess whether you have a stable income or a variable income. Based on your income stability, you may choose the premium payment option that suits you.

Financial goals: Evaluate your financial goals. Assess whether you want your insurance to be an income replacement, clear all debts and secure your child’s educational future. An insurance policy should align with your goals.

Long-term affordability: Evaluate your budget to ensure it does not affect your daily expenses and is suitable for long-term affordability.

Final Thoughts

Choosing between limited pay and regular pay in term insurance depends on your financial stability and the life goals you have set for yourself and your family.

If you currently have a higher income and wish to finish the payments early, you may consider a limited pay option. However, if you feel you can make regular payments throughout the policy tenure, you may choose regular pay premiums.

Frequently Asked Questions

Below are some of the frequently asked questions on Limited Pay vs Regular Pay in Term Insurance: Key Differences Explained

Can I switch from regular pay to limited pay in term insurance?

Most insurance companies in India do not allow switching from regular pay to limited pay in term insurance once the insurance is issued. Thus, you need to take the decision before you purchase the policy.

Is limited pay better than regular pay in term insurance?

Which one is better depends on your financial stability. If you have a higher income in early life, you may choose limited pay. However, if you want to spread premium payments over the policy term, regular pay may be suitable.

Always read the pros and cons of both term insurance premium payment options before making a decision.

Does limited pay term insurance have higher premiums?

Yes, limited pay term insurance usually has higher premiums than regular pay. It is because you are paying for the same coverage within a shorter period.

Who should choose regular pay in term insurance?

Regular pay may suit individuals who prefer smaller premium payments spread across the entire policy term. It may also work for people with stable long-term income who want to manage their expenses gradually.

What happens if I stop paying premiums under a limited-pay plan?

If you stop paying premiums under a limited pay plan, the policy may lapse if premiums remain unpaid. Also, the benefits may be affected, subject to policy terms.

How do insurers calculate premiums for limited pay vs regular pay plans?

Insurers calculate premiums by assessing risk factors such as age, health, policy term, and coverage amount. The main difference between calculating limited vs regular pay is how they spread the risk and the associated costs over time.

Explore Life Insurance Product

Was this article helpful?

Recent

Articles

Do ADAS Features Reduce Car Insurance Premiums in India?

Nikhila PS Jun 25, 2026

How Do BS6 Bikes Affect Bike Insurance Premiums and Coverage?

Nikhila PS Jun 25, 2026

Does Health Insurance Cover Recurrent Depressive Disorder?

Neviya Laishram Jun 25, 2026

Top 15 Car Companies in India in 2026

Nikhila PS Jun 25, 2026

Does Two-Wheeler Insurance Cover Dents and Paint Damage?

Nikhila PS Jun 24, 2026

All Articles

Want to post any comments?

ACKO Term Life insurance reimagined

ARN:L0072|*T&Cs Apply

Check life insurance

#36/5, Hustlehub One East, Somasandrapalya 27th Main Rd, Sector 2, HSR Layout, Bengaluru, Karnataka 560102