ResourcesExplore the full ACKO experience and make the most of your plan

EXPLORE

Articles

Guides

Ebooks

Enterprise

Enterprise

Support

Support

Term insurance

Term insurance is the purest type of life insurance. A term insurance plan offers financial protection for a fixed period in return for a regular premium. The money your nominee receives as a payout (called the death benefit) can help cover important costs such as your children’s education, healthcare expenses, and daily needs like food and clothing.

Term insurance is the purest type of life insurance. A term insurance plan offers financial protection for a fixed period in return for a regular premium. The money your nominee receives as a payout (called the...

Term insurance is the purest type of life insurance. A term insurance plan...

What are the benefits of buying a term insurance plan?

Length of Policy and Sum Assured

2. Gender: Women Pay Less

3. Smoking and Tobacco Use

What is the definition of a smoker by insurers?

Health and Medical History

5. Occupation and Lifestyle

How to Buy Term Insurance Online?

Differences between Term Insurance and Other Life Insurance Types

What are the best term insurance plans in India 2025?

Who Should Buy a Term Plan?

Why Choose ACKO for Your Term Insurance Plan?

Is ACKO a trustworthy company for term insurance?

Key Features of Term Insurance

6 Key Life Situations to Purchase Term Life Insurance

A Complete Guide to the ACKO Life Flexi Term Plan

Best Term Insurance Plans for 2025

ACKO Term Plan: Inflation Protection & Cost Savings Option

How to Choose the Best Term Insurance in India?

Choose the Best Term Insurance Plan as Per My Needs

How Does a Term Plan Secure Your Family's Future?

How Much Term Cover Do I need?

Importance of Sum Assured in Term Insurance

What is the Ideal Duration of Term Life Insurance?

How to Reduce My Term Insurance Premiums?

Is the Premium for Term Insurance Different When Purchased Directly from the Company or a Broker?

What are the Payout Options in Term Life Insurance?

What are Term Insurance Riders?

Top 3 Riders for ACKO Life Flexi Term Plan

Why are Term Insurance Riders Important?

Eligibility Criteria To Buy a Term Insurance

What is Covered and Not Covered in Term Insurance?

Common Mistakes to Avoid

Why Should I Buy Term Life Insurance Online?

How to Buy Term Insurance Online?

Documents Required To Buy Term Life Insurance Plan

What are the Documents Required for Term Life Insurance Claim Process?

Why Customers Trust Our Term Insurance

Term Insurance Terminology

Find the Best Term Insurance Based on Your City

FAQs

Download ACKO Life Flexi Term Plan Policy Wording

What is Term Insurance?

Term insurance is the purest and most affordable form of life insurance. It is because a term insurance plan provides financial protection for a specific period in exchange for a fixed premium. It focuses purely on protecting the financial needs of your dependents in your absence. This means there is no investment or savings component, which is why term insurance premiums are cheaper.

In simple terms: You pay a fixed premium for a specified period (term), and if you pass away during this time, your family receives the sum assured (death benefit). If you survive the policy term, there's no payout.

Key Characteristics of Term Life Insurance

Pure protection: No maturity benefits or cash value accumulation

Fixed premiums: Premium amount remains constant throughout the policy term

Flexible tenures: Choose coverage from 10 to 40 years

Tax benefits: Save up to ₹54,600* on your taxes for under Section 80C, death benefits are tax-free under Section 10(10D) of the Income Tax Act

Zero-GST: The GST on term insurance premiums has been reduced from 18% to 0%. This means your individual term plans are completely GST-free

Get a 1 crore term insurance plan starting @₹18/day*

Why Choose ACKO Term Insurance Plan?

ACKO’s term insurance comes with flexible, customisable features that support different life stages and financial goals. It gives you everything you need to protect your loved ones and plan for the future.

Categories

Specifications

Sum Assured

₹10 Lakhs to up to ₹90 Crores

Entry Age

From 18 years to 65 years

Tax Benefits

Save up to ₹54,600* on taxes

Claim Settlement Ratio

99.29%

Affordable Premiums

Term Life Cover Starting @ just ₹18/day*

Claim process

Fully digital, simply upload the necessary documents on the app.

Death Benefit

Available

Critical Illness Cover

Available

Accidental Total Permanent Disability

Available

Accidental Death Benefit

Available

100% Dedicated Claim Assistance

Available

Policy Term Flexibility

Available

Customisable Policy Coverage

Available

Why Term Insurance is Important

According to the latest IRDAI annual report, life insurance penetration in India fell to 2.8%, down from 3% in 2022-23*. The decline reflects an increased protection gap, which means a large portion of the population is financially unprotected from life's uncertainties.

Here are some of the financial realities if you do not have a term insurance plan

Outstanding home loan: ₹50 lakh with 15 years remaining

Children's education: ₹30-40 lakh, required in the next 10-15 years

Without term life insurance, your family could face

Loss of regular income

Selling property or assets to clear debts

Interrupted education plans for children

A reduced standard of living

Financial dependence on relatives

Term insurance helps prevent all this by ensuring your family’s financial stability even in your absence.

The Mathematical Logic: The Simplified Calculation of Term Insurance

Let's see the way term coverage works in practical terms:

A 30-year-old non-smoker can get ₹1 crore term insurance cover for around ₹8,000-₹10,000 per year. Over 30 years, that’s just ₹2.4-₹3 lakh total premium in exchange for ₹1 crore life cover.

Total premium paid: Approx. ₹2.5 lakh (over 30 years)

Life cover (death benefit): ₹1 crore

Total protection value: Approximately a 4000% return on protection

The right time to buy a term insurance plan is as early as possible, because the earlier you buy, the cheaper it is and the longer your family stays protected. When you wait even 5-10 years to buy term insurance, your premium can increase by thousands, and you will have a shorter number of years of protection.

Types of Term Insurance Plans in India

There are various types of term insurance available. But are they all similar? Definitely not. Let's understand the major types of term insurance plans in India.

Plan Type

Maturity Benefit

Best For

Coverage Pattern

Pure Term (Level)

None

Everyone

Fixed throughout

Term with Return of Premium

100% premiums back

Risk-averse individuals

Fixed throughout

Increasing Cover

None

Young professionals

Increases periodically

Decreasing Cover

None

Loan protection

Decreases over time

Convertible Term

None

Uncertain needs

Fixed, can convert later

1. Pure Term Insurance Plan (Level Term Insurance)

This is the most basic and popular type of term plan where the sum assured remains fixed throughout the policy term.

Features:

Fixed death benefit for the entire policy term

Lowest premium among all types

Simple and understandable

Best for: Anyone looking for inexpensive life coverage without additional features.

2. Term Insurance with Return of Premium (TROP)

TROP provides life cover and also returns all your premiums if you survive the policy term.

Features:

Get back 100% of premiums if you outlive the term

The premiums are higher, about 1.5 to 3 times more expensive than pure term plans.

Best for: People who want life protection along with the assurance of getting their money back at the end of the term.

3. Increasing Cover Term Plan

With an increasing term insurance plan, your coverage automatically increases every year to keep pace with inflation or growing responsibilities.

Features:

The coverage increases by a fixed percentage, usually between 5% and 10% annually.

Helps cover future needs as your income and expenses grow

Premium usually remains the same or increases slightly.

Best for: Young professionals who expect their income, lifestyle, and financial needs to increase over time.

4. Decreasing Cover Term Plan

With a decreasing term insurance plan, your coverage amount decreases gradually during the policy term, matching your loan balance.

Features:

Good option to cover liabilities like home or business loans

Lower premiums as compared to regular term plans

The coverage decreases as your outstanding debt goes down.

Best for: Borrowers who want protection for large loans that reduce over time.

5. Convertible Term Plan

It allows you to convert your term plan into a whole life or endowment policy later, without the requirement of any medical tests.

Features:

Easily convert to a permanent life insurance plan

No fresh medical check-up needed

Useful if your long-term financial goals change

Best for: Individuals who are unsure of their needs in the future and would like flexibility to switch plans later.

6. Group Term Life Insurance

It is a term life insurance policy provided by the employer to employees as an additional benefit.

Features:

Employer pays the premium

Coverage is usually 3-5 times your annual salary

No medical test needed for basic cover

Coverage ends when you leave the company

Best for: Employees desiring basic life insurance through their workplace.

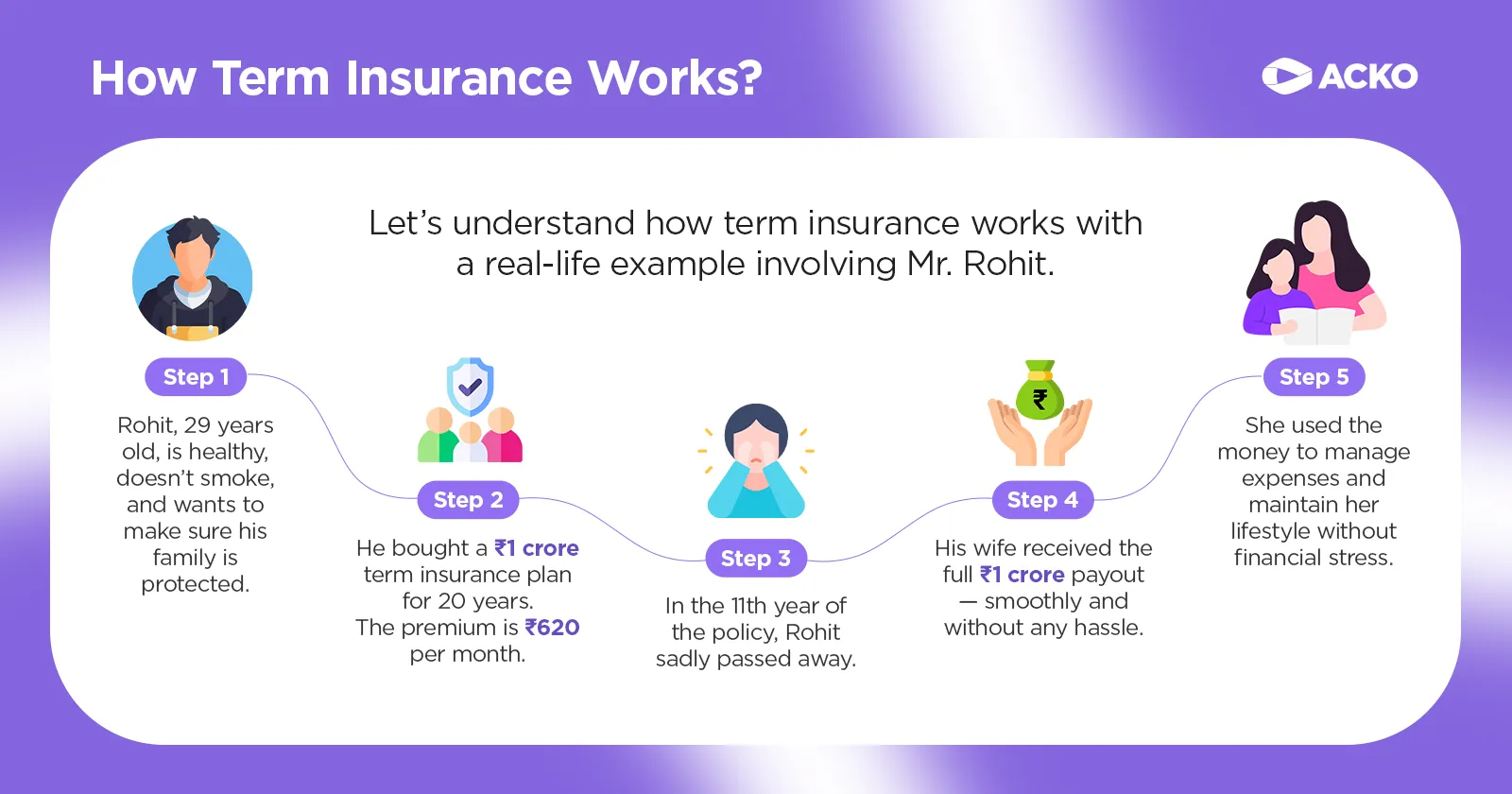

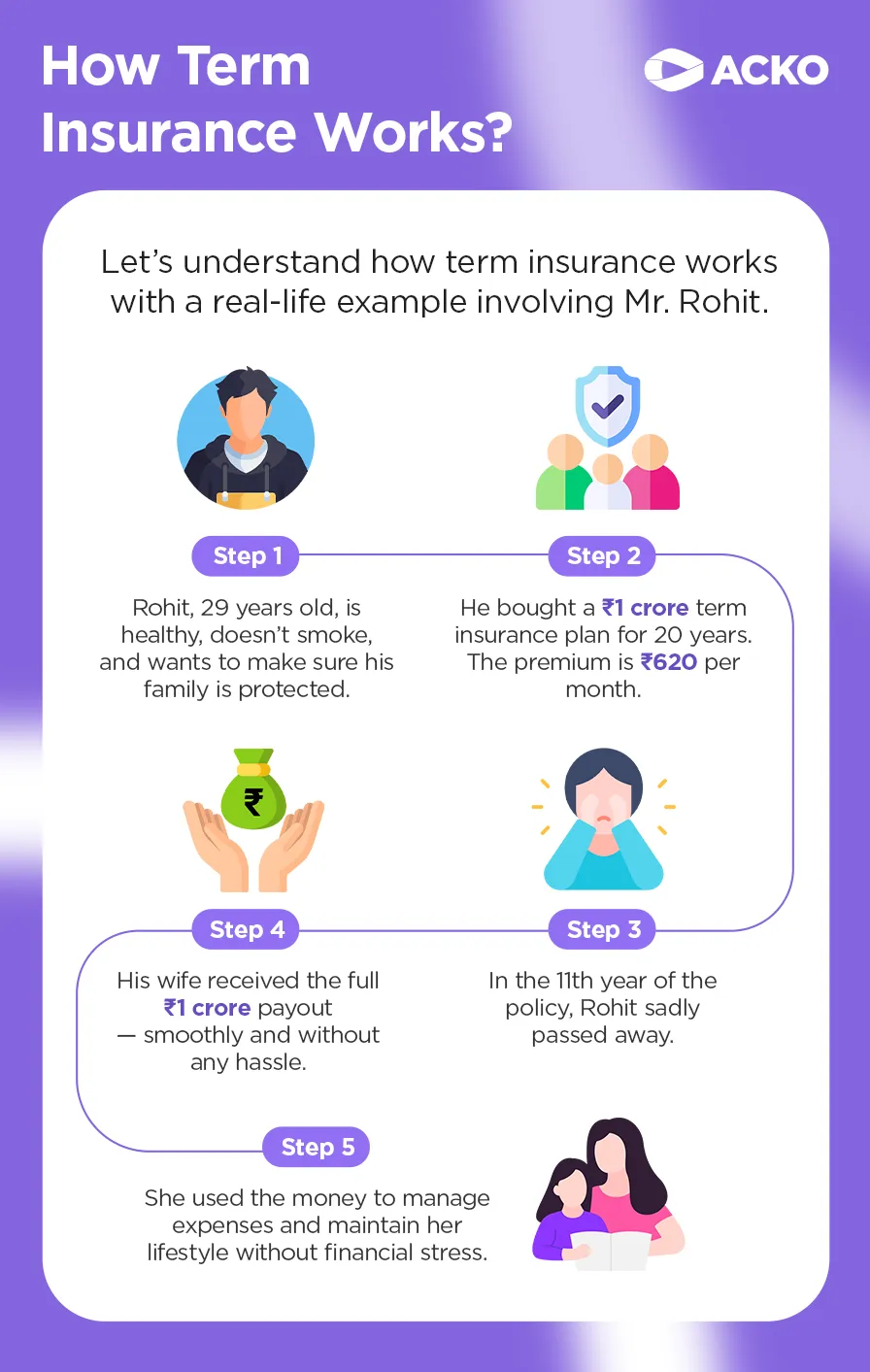

How Term Insurance Works: Step-by-Step Process

Let’s understand how term insurance works in the simplest way possible. All you need to do is follow these simple steps to see how a term plan protects your family:

Determining Your Coverage Need

The first step is to figure out how much term insurance coverage you actually need. The coverage amount is also known as the sum assured (the money your family would receive if you pass away). So, it’s one of the most important decisions because it directly affects your family’s financial security and also your policy premium.

When calculating the right coverage amount, there are two simple ways to estimate your needs:

A. Human Life Value Method: Annual Income × Number of working years remaining Let’s say you’re 35 years old and earn ₹12 lakh per year. You plan to retire at 60, which means you have 25 working years left. According to the Human Life Value (HLV) method, your ideal life insurance cover would be: ₹12 lakh × 25 years = ₹3 crore

B. Needs-Based Calculation: Your life insurance cover is calculated based on your family’s financial needs and goals. So, here’s how it works: Coverage needed = Total Financial Obligations + Emergency Fund + Future Goals

Example: Understanding the Needs-Based Calculation

The next thing you’ll want to do is choose how long you want your term insurance coverage to last. The policy term means how many years your plan will provide protection, and there are some simple ways to decide this:

Until retirement: This is the most common choice (e.g., 30-year term for a 30-year-old)

Until a major financial goal has been reached, such as children's education or home loan repayment.

Until dependents become financially independent: 20-25 years.

Now that you have determined your term insurance coverage and policy term, your next step is to choose your premium payment option. The premium payment option can impact your budget, payment convenience, and long-term financial planning; thus, it is best to choose a premium payment option that you are comfortable with. You can choose either:

1. Regular Pay:

Pay monthly, quarterly, or yearly throughout the policy term.

Many people prefer the annual payment option because it offers convenience and may come with small savings.

It is suitable if you have a steady, ongoing income.

2. Limited Pay (10-15 years):

Pay for a shorter duration and get life coverage for the entire policy term.

Higher annual premium but lower total outgo

Suitable for high-income earners

Example comparison for ₹1 crore term insurance for a 30-year term:

Regular pay: ₹10,000/year × 30 years = ₹3 lakhs total

Limited pay (15 years): ₹18,000/year × 15 years = ₹2.7 lakhs total

Medical Underwriting

When you buy a term insurance plan, you’ll need to go through a quick medical check-up. This step is called medical underwriting. This is an important step of the process because it ensures your premiums are based on your actual health conditions.

Process:

Fill out a detailed health questionnaire

Basic plans up to ₹50 lakhs: May not require medical tests

Higher coverage like 1 crore term insurance required: Blood test, urine test, ECG and more.

Note: Always disclose your complete medical history to avoid future claim complications.

Policy Issuance

Once your application and medical underwriting are done, your term insurance policy is issued. This is when your coverage officially starts, and you will receive your policy document (digitally or physically) with all the details about your plan.

A. Free Look Period: After receiving your policy, you get a free look period to review it carefully. Use this time to:

-Read all terms and conditions -Verify coverage details -Check nominee information -Cancel if not satisfied (premium refunded minus administrative charges)

B. Grace Period: In case you miss a premium payment, most insurers offer a grace period. Grace period details:

-Monthly payments: 15 days -Quarterly, half-yearly, or annual payments: 30 days

Why Should I Buy Term Insurance in 2025?

There are many reasons to buy term insurance in 2025. When you look at term insurance benefits, from how it protects your family to supporting children’s education and covering loan repayments, you see why it is so important.

Here’s why you should consider getting a term plan in 2025:

To protect your family/loved ones: One of the most important term insurance benefits is that it provides money to your family if you pass away. The death benefit helps your spouse, children, or parents manage daily expenses and future needs without financial trouble.

To protect your home and assets: Loans like home loans or car loans can put pressure on your family if you are not there. A major benefit of term insurance is that it helps clear these debts, so your loved ones don’t have to worry about repayments.

To maintain your family’s lifestyle: Another valuable term insurance benefit is that it helps your family manage daily living costs. If you earn a salary and have dependents, the payout in your absence ensures they don’t have to compromise on their standard of living. This support gives them stability during difficult times.

To get a large coverage amount by paying easily affordable premiums: A term insurance policy gives a large death benefit at very low premiums. At ACKO, life cover starts @ just ₹18/day*. This makes it an easy and smart way to protect your loved ones. Remember, term insurance is the simplest type of life insurance and is meant only for pure protection.

To be prepared for life’s sudden challenges: Life can bring sudden challenges. Events like accidents or serious illnesses may be beyond your control. According to the ACKO Accident Index 2024, 78% of road accidents in India happen in metro cities. The most accident-prone cities include Hyderabad and Delhi NCR, followed by Pune and Bengaluru. On the other hand, critical illness treatments can cost several lakhs, with medical inflation rising yearly. Having a term plan is about caring for your loved ones and making sure your family is protected from future financial challenges due to loss of income.

To get extra protection with useful riders: Everyone has different needs, and term insurance can be customised with riders for extra protection. For example, you can choose riders for critical illness, accidental death, disability income, etc. This makes your term insurance plan more useful by covering more than just life protection.

To get tax benefits: Another term insurance benefit is that you can save on taxes. The premiums you pay are eligible for deductions under Section 80C of the Income Tax Act, depending on the tax regime you choose. Also, the payout your family receives is usually tax-free under Section 10(10D).

What are the benefits of buying a term insurance plan?

Below are some of the main benefits associated with term insurance:

1. Huge Coverage at Low Cost

Among all life insurance products available, term insurance provides the highest coverage at the lowest premium.

Comparative costs (aged 30 male, ₹1 crore cover):

Term insurance: ₹8,000-10,000/year

Traditional endowment plan: ₹3-6 lakh per year (estimated range for ₹1 crore cover; varies by insurer and policy term)

According to the latest IRDAI report on life insurers in 2025, life insurers in India settled 96.82% of claims in 30 days in FY 2023-24. This indicates how families can access financial support when they need it.

Here’s how term insurance helps your loved ones in real life:

Gives immediate money to manage funeral or emergency expenses

Helps your family repay loans like home or personal loans

Acts as an income replacement for the next 10-15 years

Keeps your children’s education plans secure

Ensures your spouse’s retirement plans remain safe and steady

3. Tax Benefits: Dual Advantage

Section 80C Benefits: Premiums paid are deductible up to ₹1.5 lakhs annually.

Section 10(10D) Benefits: Tax-free death benefit to nominees.

4. Debt Protection

According to the Financial Stability Report by the RBI, household debt went up to 42% of GDP in 2024 from 26% in 2015, indicating a rise in financial liabilities. Household debt refers to the total amount of money families owe to banks or financial institutions, which includes home loans, car loans, education loans, personal loans, and credit card loans.

How term insurance helps:

Prevents a forced sale of property

Protects co-borrowers from the burden

Maintains the credit score of the surviving family members

5. Peace of Mind

Term insurance removes that persistent thought in the back of one's mind: "What would happen to my family were I not around?" Here's how such peace of mind helps in daily life:

If you're less stressed about the future, you can then focus more on your career and goals.

When you feel secure, it leads to stronger and happier family relationships.

You can plan long-term without fear of leaving unfinished responsibilities.

6. Flexible Payout Options (Death Benefit)

Choose how your family receives money:

a) Lump Sum:

The whole amount in one payment

Suitable for immediate debt clearance

Requires financial discipline

b) Income Benefit (Instalments):

Monthly/annual payouts for a specified period

Example: ₹1 crore as ₹50,000/month for 20 years

Ensures steady income flow

Prevents the misuse of a large amount

c) Combination:

50% in lump sum + 50% in installments

Immediate needs + long-term security

Which Factors Affect Term Insurance Premiums?

Several key factors affect premiums for term insurance plans. Some of them include your age, health, lifestyle habits, coverage amount, and policy duration.

Length of Policy and Sum Assured

The length of your insurance policy will also affect the premium. A longer policy term will attract higher premiums than a shorter policy term. Let’s say a 30-year-old buys ₹1 crore cover:

Policy Term

Premium & Total Cost

20-year term

₹7,500/year = ₹1.5 lakhs total

30-year term

₹8,500/year = ₹2.55 lakhs total

40-year term

₹10,200/year = ₹4.08 lakhs total

Age

Your age plays a big role. The younger you are when you buy a term insurance policy, the lower your premium will be. Let’s understand this better with an example. The table below shows how premiums change based on your age at purchase and how buying early can save you thousands of rupees.

Purchase Age

Annual Premium (₹1 Crore, till age 60)

Total Premiums Paid

Years of Coverage

25 years

₹7,200

₹2,52,000 (35 years)

35 years

30 years

₹8,500

₹2,55,000 (30 years)

30 years

35 years

₹11,800

₹2,95,000 (25 years)

25 years

40 years

₹17,500

₹3,50,000 (20 years)

20 years

45 years

₹28,000

₹4,20,000 (15 years)

15 years

Gender

Studies indicate that women, on average, live longer than men. Thus, women typically pay lower premiums due to higher life expectancy. Let’s say a 30-year-old buys ₹1 crore cover:

Age

Coverage

Male (Non-smoker)

Female (Non-smoker)

Savings for Women

% Difference

25

₹1 crore (30-yr)

₹7,200

₹6,100

₹1,100/year = ₹33,000 lifetime

15%

30

₹1 crore (30-yr)

₹8,500

₹7,200

₹1,300/year = ₹39,000 lifetime

15%

35

₹1 crore (25-yr)

₹11,800

₹10,200

₹1,600/year = ₹40,000 lifetime

14%

40

₹1 crore (20-yr)

₹17,500

₹15,200

₹2,300/year = ₹46,000 lifetime

13%

Disclaimer: Premiums are approximate averages for healthy, non-smoking individuals. Actual premiums vary by insurer, policy term, health status, and any selected riders.

Smoking and Tobacco Use

Because of your increased mortality risk, smoking and tobacco use greatly raise your premium.

Age

Coverage

Non-Smoker Premium

Smoker Premium

Extra Cost for Smoking

Lifetime Extra Cost

25

₹1 crore (30-yr)

₹7,200

₹10,500

₹3,300/year

₹99,000

30

₹1 crore (30-yr)

₹8,500

₹12,500

₹4,000/year

₹1,20,000

35

₹1 crore (25-yr)

₹11,800

₹17,200

₹5,400/year

₹1,35,000

40

₹1 crore (20-yr)

₹17,500

₹26,000

₹8,500/year

₹1,70,000

What is the definition of a smoker by insurers?

To insurers, “smoker” means not just someone who smokes cigarettes. It includes someone who consumes any form of nicotine.

This includes:

Cigarettes, cigars, pipes

Chewing tobacco, gutka, paan masala

Electronic cigarettes

Any other form of consumption of nicotine

Health and Medical History

Your current health and your medical history have a big impact on your premiums. Here are some of the conditions that will affect your premiums:

Minor impact (0-15% loading)

Moderate impact (15-50% loading)

Significant impact (50%+ loading or decline)

Controlled diabetes

Obesity (BMI > 35)

Cancer history

Managed hypertension

Cholesterol issues

Multiple heart attacks

Previous minor surgeries

Past heart conditions

Chronic kidney disease

Thyroid disorders under control

Asthma

HIV/AIDS

Occupation and Lifestyle

Your profession and lifestyle activities affect your risk profile and premium rates.

Risk Category

Occupations

Premium Loading

Special Conditions

Standard Risk

Office workers, teachers, IT professionals, doctors, and accountants

Field engineers, journalists, sales executives (extensive travel)

10-15% loading

May require additional questionnaire

High Hazard

Pilots, defence personnel, mining workers

20-40% loading

Special exclusions may apply

How to Buy Term Insurance Online?

The process to buy a term plan is simple and straightforward. Follow the steps below:

Compare Multiple Insurers

Choose insurers with proven track records of settling claims quickly and fairly.

Check coverage features

Read customer reviews

Calculate Coverage Requirement

Use online premium calculators:

Enter age, income, and location

Specify financial obligations

Add future goals

Get recommended coverage

Get Instant Quotes

Information needed:

Date of birth

Gender

Annual income

Smoking status

Coverage amount

Policy term

Online quotes are cheaper than offline ones due to:

No agent commission

Lower operational costs

Direct digital processing

Fill Application Form

Personal details:

Full name, address, contact

PAN card (mandatory above ₹50,000 annual premium)

Aadhaar card

Income proof

Medical details:

Height, weight (BMI calculation)

Medical history

Family medical history

Lifestyle habits

Upload Documents

Having the right documents ready makes your term insurance application process quick and smooth. Here’s a simple list of documents required to buy term insurance.

Age Proof (Birth certificate, PAN, Aadhaar, or Passport)

Identity Proof (Aadhaar, Passport, or Driving License)

Address Proof (Aadhaar, Utility Bill, or Passport)

PAN Card

Income Proof (Salary slips, Form 16, or ITR)

Passport-size Photograph

Medical Reports

Bank Account Details (Cancelled cheque)

3 Years ITR

Net Worth Statement

Medical Tests (if required)

The medical tests required depend on your age and the coverage amount you're applying for. Some of the common term insurance medical tests include:

Tip: Pay annually to save compared to monthly payments

Policy Issuance

Receive policy via:

Email (soft copy)

Registered mail (physical copy)

Download from the insurer portal

Differences between Term Insurance and Other Life Insurance Types

Here’s how term insurance differs from other life insurance options.

Feature

Pure Term Insurance

Term with ROP

Endowment Plan

ULIP

Whole Life

Primary Purpose

Pure protection

Protection + premium return

Protection + savings

Protection + investment

Lifelong protection

Coverage Amount (for ₹10,000 premium)

₹1 crore

₹60-70 lakhs

₹10-12 lakhs

₹15-20 lakhs

₹30-40 lakhs

Maturity Benefit

None

Premiums refunded

Guaranteed maturity value

Market-linked fund value

Yes (at age 99-100)

Returns

N/A

0% (money back)

4-6% (bonus-based range)

8-12% (depends on fund performance)

4-5%

Lock-in Period

None

Full term

Full term

5 years

Full term

Recommended For

90% of people

Risk-averse savers

Forced saving needed

Want market exposure

Estate planning, HNIs

What are the best term insurance plans in India 2025?

Below are some of the most common and widely chosen term insurance plans in India.

Type of Term Plan

Benefits

Term Insurance

Gives your family money if something happens to you. It’s the simplest and most affordable type of life insurance.

Term Insurance with Return of Premium (TROP)

Protects your family, and if you live through the policy term, you receive a refund of all the premiums you paid.

Term Insurance with Accidental Death Cover

Gives your family extra money if you pass away due to an accident.

Term Insurance with Waiver of Premium Rider

If you can’t work due to a disability or illness, you don’t have to pay future premiums, but your policy still continues.

Term Insurance with Critical Illness Rider

Along with life cover, you get a lump sum if you’re diagnosed with a serious illness like cancer or a heart problem. Helps pay for medical treatment.

Term Insurance with Disability Income Rider

Gives you a regular monthly income if you become permanently disabled and can’t work. Helps cover daily expenses.

Increasing Term Insurance Plan

Your coverage grows every year to keep up with inflation and future expenses. Great for young earners and growing families.

Who Should Buy Term Insurance in 2025?

Buying a term insurance plan is a practical option for everyone, especially those who are financially dependent, to secure their family’s finances in case something unfortunate happens. Here’s a list.

Young and Healthy People: Buying term life insurance when you're young and healthy can be cheaper. It's like locking in a good deal for the future.

Earning Members: If you're the one who earns for your family, term life insurance is essential. It ensures your family won't face financial difficulties if you're no longer there to support them.

People with loans or EMIs: If you have loans or debts, like a home/personal/car loan, term life insurance can cover those debts so your family doesn't get burdened.

Taxpayers: If you're looking to save on income tax while securing your family's future, term life insurance is a smart choice. Premiums paid are eligible for tax deductions under Section 80C, and the payout to your family is tax-free under Section 10(10D).

Homemakers / Non-Working Spouses: Homemakers play an important role in running the household and supporting the family. Term insurance for non-working spouses helps ensure that daily needs like childcare, groceries, and household support are taken care of, in case of an unforeseen event.

Working Women: In today’s workforce, women stand shoulder-to-shoulder with men. Term insurance for working women offers tax savings and helps secure a family's financial future. Additionally, many plans include riders, such as critical illness coverage, for life-threatening illnesses commonly affecting women.

Newly Married Couples: When you're beginning your married life, term insurance provides financial protection for your spouse in case something happens to you. Buying early also means lower premiums.

Single Parents: If you're a single parent, your children depend on you entirely. Term life insurance can give you peace of mind, knowing that your kids will have financial support if something happens to you.

Estate Planners: If you want to leave your heirs and inheritance or financial legacy, term life insurance can help ensure they receive it.

Business Owners: If you own a business, term life insurance can be crucial to ensure the smooth transition of your business or to cover business debts in case something happens to you.

People with Ageing Parents or Dependents: Many Indians support their parents or siblings financially. A term plan ensures that your dependents won’t be left helpless in your absence.

Why Choose ACKO for Your Term Insurance Plan?

ACKO keeps term insurance simple. You can buy it online and manage everything in the app. With ACKO Term Insurance, you get protection that’s cheaper, faster and smarter. It’s built for the digital world, so you spend less time on paperwork and more time with the people you love.

Low premiums with Zero GST: ACKO offers 1 crore term insurance starting at ₹18/day. With GST now removed from all individual term insurance premiums, you save more on your overall premium.

Simple, fully digital experience: You can buy, manage, and update your policy completely online. No paperwork, no branch visits, everything is handled through the ACKO app.

Coverage that adjusts based on needs: Whether your responsibilities increase or you want longer protection, you can easily change your sum assured or policy term whenever you need.

Quick and easy policy updates: From updating your address to adding riders or changing your nominee, all your policy changes can be done in minutes from the app.

Strong claim performance: With a 99.29% claim settlement ratio, ACKO’s term insurance gives your family reliable financial protection.

Add-on riders for extra protection: You can customise your plan with riders like critical illness cover, accidental death benefit, and disability income to suit your needs.

No hidden charges: ACKO’s direct-to-customer digital model keeps everything transparent. Since there are no agents, you avoid extra spending and get a plan that’s simpler and more cost-effective.

Fast claim process: Your nominee can file a claim online with clear guidance at every step. This makes the entire experience quicker and stress-free.

Is ACKO a trustworthy company for term insurance?

Yes. ACKO Life is a fully IRDAI-licensed insurer with a claim settlement ratio of 99.29% and a strong digital-first service model. There’s no paperwork; you can do it anytime on the app, and a support team is always ready to help.

Backed by proven expertise: ACKO General Insurance has served over 78 million customers with an excellent claims settlement ratio. ACKO Life continues this focus with a strong ACKO Life Insurance Claim Settlement Ratio - May 2025

Dedicated support team for fast claim processing – Submit the required documents to our support email at [email protected] or simply dial 18002101992. The ACKO claims team will take care of the rest.

What are the Key Features of Term Insurance?

Term insurance is affordable, easy to understand, and offers a low entry age and debt protection. It also provides flexible premium payments, customisable coverage, and payout options. Here’s a quick look at the key features and benefits of term insurance plans.

Low Entry Age: You can get term insurance from age 18. Starting early means lower premiums and longer coverage.

Long Term Protection: Term insurance provides coverage for a stated or specified period, such as 10, 20, or 30 years. If the insured lives beyond the stated term, then the policy expires and pays no benefit.

Simplicity & Easy to Buy: Term insurance is quite simple in nature, making it easier to understand and purchase compared to other types of life insurance.

Easy Premium Payment Options: You can choose how you want to pay premiums: monthly, quarterly, yearly, or even once. Choose what works best for you.

Customisable Coverage: The amount of coverage can be increased or decreased in most cases according to your needs and financial responsibilities (e.g., paying off a mortgage or dependents).

Affordability: Term insurance is usually more affordable than whole life or universal life because it does not include a saving or investment component. The premiums are normally lower.

Convertibility: A conversion option means that you may convert your term policy into a permanent life insurance policy, such as whole life or universal life, without showing evidence of insurability. This is particularly useful if your health changes or you decide later in life that you might want lifetime coverage.

Fixed Premiums: When paying for term insurance, the premiums are fixed for the duration of the term. That is to say, the amount paid for protection is constant throughout the term. Hence, locking in these premiums early in life is a smart financial move.

Renewability: There are term insurance policies that allow renewal of the policy after the term is over, generally at an increased premium. The good thing here is that you can extend the coverage without a new medical exam, although the premium will surely increase as you get older.

Payout Options: Multiple payout choices for how your beneficiaries receive the money in case of your ultimate demise.

Death Benefit: When the policyholder dies during the period known as the 'policy term,' a tax-free death benefit is paid to their named beneficiaries.

No Cash Value: Term insurance does not build any cash value or investment component; it is purely a protection policy designed to pay a death benefit.

6 Key Life Situations to Purchase Term Life Insurance

Choosing the best term life insurance at the right moment can make all the difference. Discover 6 important life scenarios where purchasing term insurance is a wise financial decision.

Health Conditions: If you are in good health, purchasing term life insurance is generally easier and more affordable. The longer you wait, the more health problems you may have, which means the more you may have to pay, or you might not get coverage at all.

Starting a Family: Term life insurance would ensure that your spouse, children, or other dependents are protected to preserve their standard of living in case of anything adverse.

Taking on Debt: Large debts, such as a mortgage or car loan, can be paid off upon one's death through term life insurance policies, thus avoiding financial burdens on the family.

Growing Your Family: With each addition to the family comes an increase in financial responsibilities. Life insurance will help provide for future expenses and protect your family's future financially.

Changing Jobs or Careers: A job change, especially an upgrade in salary or increase/decrease in responsibilities, could be an opportune time for reviewing life insurance needs.

Estate Planning: As you begin considering estate planning, term life may become a convenient way to pay estate taxes or other costs that come due upon your death.

Best Term Insurance Plan in India 2025 by ACKO Life

ACKO Life Flexi Term Plan is a modern, flexible, and customer-centric solution for long-term financial protection. It not only offers inflation protection through premium lock-ins but also provides a unique level of policy flexibility unmatched by most traditional insurers. The convenience of managing the entire policy lifecycle digitally adds to its appeal, particularly for individuals who prioritise ease of use and adaptability.

ACKO offers a fully digital policy management system. Policyholders can easily make any policy adjustments (endorsements) such as:

Many traditional insurers require offline, time-consuming processes for policy adjustments, often involving paperwork or visits to branch offices. ACKO’s completely digital process offers unmatched convenience, especially for tech-savvy consumers.

Understand the Flexibility of ACKO Life Flexi Term Plan

The ACKO Life Flexi Term Plan starts at just ₹18/day*, and adapts as your life changes. Watch this video to learn everything you need to know about ACKO’s Term Insurance Plan.

ACKO Term Insurance Plan vs Traditional Term Plans

Looking for the best term insurance in India 2025? Buy one of India’s best term insurance plans starting at just ₹18/day. With ACKO Term insurance, you get complete flexibility to customise your coverage amount and policy term to match your changing life goals.

The table below compares the ACKO Term insurance Plan with traditional term insurance plans, highlighting key differences in flexibility, premium payment options, and value-added features, so you can decide which is the best term insurance plan in India 2025 for your needs.

Parameters

ACKO Life Flexi Term Plan

Traditional Plans

Claim Settlement Ratio

99.29%

Varies from 98-99%

Policy Adjustments

Instant changes via app

Depends on the medium ( offline and online )

Increasing Cover Option

Yes. No restrictions*

Restricted to life's big events such as marriage, welcoming a child, etc.

Cost Savings

Up to 40% savings*

Costs grow over time

Future Premium Hikes

Age-wise premiums remain the same

Age-wise inflation-adjusted premium

Customisability

Flexible coverage/term

Rigid, limited options

Riders

Offers valuable riders to enhance protection

Riders may be provided, depending on the plans

Length of Claim Form

Easy, digital, and short

Moderately long/Very long/Not available online

Option to Exit the Plan

Yes*

Approx. 80% of insurers provide

Digital Experience

Fully online, app-based 📱

Often requires offline processes, paperwork, or branch visits

End-to-end Digital Support

Yes

Depends on the insurer

Free Will Creation

Yes

No, Generally does not offer integrated will creation services

ACKO Life Flexi Term Plan: Inflation Protection and Cost Savings Option in 2025

When you first buy ACKO’s Flexi Plan, the premium rates for different coverage amounts are fixed based on your age at the time you start the policy.

If you're 30 years old in 2025 and buy a term plan with a ₹1 crore sum assured.

Later, in 2035, when you turn 40, you decide to increase the coverage to ₹2 crore.

The premium will be calculated as if you're a 40-year-old in 2025, not in 2035.

This protects you from paying higher premiums that would normally apply to a 40-year-old in 2035.

Market Comparison

In the last 4 years, term insurance premiums have increased by more than 40% on average. ACKO's Life Flexi Term Plan can potentially help you save up to 40% on premiums in the long run, assuming these historical price trends continue. Most market plans do not offer a similar lock-in mechanism for future premium hikes related to sum assured increases.

How to Choose the Best Term Insurance in India?

Choosing the best term insurance plan in India can feel confusing. You want something that fits your needs just right. Here are the steps to help you pick the right term insurance plan for you.

Determine your Coverage Need

Income Replacement: Find out how much income your family would require to maintain their present lifestyle if you were no longer around.

Debt Coverage: You must account for loans and other liabilities in the coverage as well.

Future Expenses: Consider future expenses like education, the marriage of children, etc., for long-term financial goals.

Select Correct Coverage Amount: The sum assured should be 15-20 times your annual income, which may vary depending on your requirements.

Select the Policy Term: Select a term that considers your financial liabilities and objectives. Standard terms range from 10 to 30 years. Ideally, you should have coverage until you're 70 years old to ensure adequate protection.

Age and Health: Your health and age would determine the premium and coverage options. The younger and healthier you are, the lower the premiums might be.

Check the Insurer's Claim Settlement Ratio: The high claim settlement ratio explains the reliability of the insurer in case of claim settlement. Research this ratio to determine the performance of the insurer. According to the IRDAI, the claim settlement ratio for the public sector insurer was 98.52% as of March 31, 2023. For private insurers, the claim settlement ratio was 98.02% for the fiscal year 2022-23. For additional details, please refer to the IRDAI Annual Report 2022-23.

Comparison of Premiums and Affordability: Look at the premiums for various plans and see which ones fit your budget. Some insurers offer flexible premium payment options, too.

Riders and Additional Benefits: Check if the policy offers riders such as accidental death benefit, critical illness cover, or even a premium waiver. These riders can provide extra protection and benefits to the insured.

Check the Reputation of the Insurer: Go through customer reviews, financials, and the reputation of the insurer in the market. Go for the one that has good customer support and service.

Understand the Terms and Conditions of the Policy: The policy document has to be read with care to understand the terms, exclusions, and conditions. Check whether there is some clause that may affect the coverage.

Professional Advice: A financial or insurance expert will help advise based on the particular situation of the individual.

Choose the Best Term Insurance Plan as Per My Needs in 2025

Choosing the right term insurance depends on factors like your age, policy duration, and salary. Here are some popular ways to choose the best term insurance plan in 2025.

1. Pick a Term Insurance Plan as per your age

Age plays a key role in deciding your term insurance premium. As you grow older, the premium amount usually increases, and your life cover needs may also change. That’s why it is important to choose the right coverage amount based on your age and financial requirements.

2. Pick a Term Insurance Plan as per the policy term

The right term (duration) for an insurance policy is based on your needs and situation. Consider a few of the following when pre-determining how long your term should last.

Financial Responsibilities: Consider how long you'll have certain financial responsibilities, such as a mortgage or dependent children. For example, if you have a 30-year mortgage, it might make sense to opt for a 30-year term policy to ensure coverage until the mortgage is paid off. It is wise to extend your coverage until you're 70 years old to ensure comprehensive protection.

Income Replacement: If, for instance, the aim is to replace income for your dependents if something were to happen to you, you may want a policy that can last until they become financially independent.

Cost vs. Coverage: Policies with longer terms generally tend to be more expensive, so balance your needs with your budget and select a policy term accordingly.

Here are some of the popular policy terms in term insurance that many people prefer.

3. Pick a Term Insurance Plan based on your Salary

Your budget is crucial in choosing the right sum assured. Ensure the premium you'll pay for the term plan comfortably fits your budget. You want to avoid straining your finances by going for a sum that's too high. Here are some popular options in term insurance for salaried individuals:

Let’s examine how term insurance can protect a family’s future using Mr. Suresh as an example, a regular, responsible family man.

Mr. Suresh was a 32-year-old software engineer living in Bengaluru. He was the sole earning member of a family of four: his wife and two young children. He had many dreams to fulfil. But life took a tragic turn when he passed away suddenly. What made all the difference was that Mr. Suresh had a ₹1 crore term insurance plan.

Now, let’s look at how that one decision protected his family’s future:

Replaced His Monthly Income: His wife received a ₹1 crore payout. This helped replace his income and cover essential expenses like rent and groceries, just like his salary did. Estimated monthly expenses for a 4-member middle-class Indian family range between ₹45,000 and ₹70,000, according to various 2024 estimates and surveys.

Cleared Outstanding Loans: Mr. Suresh had loans, like a home loan and personal/car EMIs. His term plan helped pay them off, so the family didn’t lose their home or fall into debt. With per capita borrower debt rising by nearly 23% over the past two years and non-housing debt representing around 55% of household liabilities, financial pressure on Indian families is growing.

Helped with His Children’s Education: His kids, aged 5 and 9, had money saved for school and college. Because of the term plan, they didn’t have to rely on luck or donations. As per a study covering 2014–2018, the cost of engineering education in India’s top colleges averaged ₹15–18 lakh, while MBA programs from tier 1 and tier 2 institutes ranged between ₹18–20 lakh.

Supported His Wife’s Future: His wife used some of the money to start a small business at home. This helped her earn on her own and take care of the family. Today, many women entrepreneurs in India are primary earners in their households. This reflects a strong shift toward financial independence and greater responsibility.

How Much Term Insurance Cover Do I Need?

Choosing the right term insurance cover is important. It helps protect your family’s future if something happens to you. Here’s a simple way to figure it out:

Think About Your Income: A good rule is to choose a cover that is 10 to 15 times your yearly income. For example, if you earn ₹5 lakhs a year, your cover should be around ₹50 to ₹75 lakhs.

Human Life Value: Human Life Value (HLV) is the estimated total income you would earn for your family during your working years, adjusted for inflation, liabilities, and future goals.

Why is Sum Assured an Important Factor in Term Insurance?

The sum assured is the prime factor in a term insurance policy, as it forms the actual amount the insurance company pays out to the beneficiaries in case of the death of the policyholder. Here's why it is an important factors:

Financial Security for Dependents: Term insurance provides much-needed financial support for your dependents in case you are not around. The sum assured ensures that your dependents have enough resources to meet living expenses, pay off debts, and achieve life goals with minimum disruption.

Adequacy of Cover: The selection of an adequate sum assured is of prime importance to ensure the sufficiency of cover for the family. This amount should be enough to replace your income and cover future expenses, such as children's education or mortgage payments.

Peace of Mind: Knowing your loved ones were well taken care of and that the sum assured would financially secure them would give you peace of mind.

Here are some of the most common coverage options to explore:

You want to make sure your family is financially secure if something happens to you. But you need to figure out how much coverage you need or how much it will cost. That's where a Term Insurance Calculator comes in. In simple terms, a Term Insurance Calculator helps you determine how much insurance you need and how much it will cost. It's like a virtual assistant that takes the guesswork out of protecting your loved ones financially.

Provide basic information about yourself, such as your age and gender, and how much money you want your family to receive if you pass away.

Answer a few simple questions about your habits and health conditions.

Then, the calculator does some quick maths and gives you an estimate of how much you'll pay for the insurance each month or year. It also tells you how long the coverage will last (usually a specific number of years).

What is the Ideal Duration of Term Life Insurance?

The right term for an insurance policy is based on your needs and situation. Consider a few of the following when pre-determining how long your term should last.

Financial Responsibilities: Consider how long you'll have certain financial responsibilities, such as a mortgage or dependent children. For example, if you have a 30-year mortgage, it might make sense to opt for a 30-year term policy to ensure coverage until the mortgage is paid off. It is wise to extend your coverage until you're 70 years old to ensure comprehensive protection.

Income Replacement: If, for instance, the aim is to replace income for your dependents if something were to happen to you, you may want a policy that can last up until they become financially independent or up until they are not relying on your income anymore.

Cost vs. Coverage: Policies with longer terms generally tend to be more expensive, so balance your needs with your budget and select a policy term accordingly.

How to Reduce My Term Insurance Premiums?

If you want to save money on your policy, here are some simple ways to reduce your term insurance premiums without compromising on coverage.

1. Buy Early:

Buying term insurance early helps reduce your premium because when you are young and healthy, the risk is lower for the insurer. This means you pay a smaller premium compared to buying the same plan later in life. Starting early also ensures long coverage and gives your family strong financial protection at an affordable cost.

2. Consider Existing Assets and Savings:

Consider any savings, investments, or assets your family can rely on in an emergency. Subtracting these from the required sum assured helps you decide the right coverage amount. This ensures you don’t overestimate your needs and end up paying extra premiums.

3. Compare Policies Online:

One of the best ways to reduce your term insurance premiums is by comparing policies online. Get quotes from multiple insurers, check the premium for your chosen sum assured, and review features and benefits. This helps you find the best term plan at the most affordable cost.

4. Save on Premiums by Staying Healthy:

Living a healthy lifestyle not only improves your well-being but can also help lower your term insurance premiums. Insurers often offer better rates to non-smokers and individuals with no major health issues.

5. Select Only the Riders You Need:

Adding too many riders can increase your term insurance premiums. Pick only the term plan riders that match your needs, such as critical illness or accidental death, and skip the ones that don’t apply to your situation. This way, you get the right balance of cover without overspending.

6. Reduce Premiums by Paying Annually:

Paying your premiums annually instead of monthly or quarterly can help reduce the overall cost of your term insurance plan.

What are the Payout Options Available with Term Life Insurance?

There are different payout options in term insurance to match your family's needs. Term insurance payout options can include a lump sum, monthly income, or a combination of both.

Lump Sum Payout: Your family gets all the money at once. This is the most common option available and gives them immediate access to the entire amount.

Monthly Payout: Instead of one big payout, your family receives a fixed amount every month for a set number of years. It could be 5 years, 10 years, depending on the policy details. This helps with regular household expenses

Increasing Income: The monthly amount increases every year. This helps your family handle rising prices and living costs.

Lump Sum + Monthly Income: Part of the money is paid upfront as a lump sum, and the rest is given as monthly income over a fixed period. This gives your family quick support and steady income.

Remember to choose the right death benefit payout option in your term insurance plan. To do that, first check what options your insurance company is offering. Then, think about what suits your family best. For example, do you have any loans to pay off? Who is your nominee, and can they manage money well? Accordingly, select your term insurance payout option wisely.

What are Term Insurance Riders?

A term insurance rider is an optional add-on to a term life insurance policy that offers additional benefits and enhanced coverage. There are various types of term life insurance riders available in India, such as critical illness rider, accidental death benefit rider, critical illness and more.

You can choose riders based on what you need and what you can afford. Riders cost a little extra, so pick only the ones that give you useful benefits without making the premium too expensive.

Increase Your Coverage: Add a rider to your base plan for extra protection and greater peace of mind.

Stronger Protection: Easily get financial protection against accidental death, accidental disabilities, critical illness, etc.

Meets Specific Needs: Riders are designed to match different personal and family needs under term insurance.

3 Types of ACKO Term Insurance Riders

Let's take a closer look at some of the important term riders offered by ACKO. You can easily add these unique term insurance riders to your ACKO Life Flexi Term Plan.

ACKO Life Critical Illness Benefit Rider

ACKO Life Critical Illness Benefit Rider is an extra layer of protection for your term insurance. If you get seriously ill, this rider can provide you with a large amount of money to help you through a tough time.

Another key benefit of this rider is that ACKO waives off all future premium payments due for your ACKO Life Flexi Term Plan. We cover 21 critical illnesses, including life-threatening common illnesses among women, such as breast cancer, cervical cancer, fallopian cancer and ovarian cancer.

List of Covered Critical Illnesses:

✔️ Cancer of Specified Severity

✔️ Myocardial Infarction (First Heart Attack Of Specific Severity)

✔️ Open Chest CABG

✔️ Open Heart Replacement Or Repair Of Heart Valves

✔️ Coma Of Specified Severity

✔️ Kidney Failure Requiring Regular Dialysis

✔️ Stroke Resulting In Permanent Symptoms

✔️Major Organ /Bone Marrow Transplant

✔️ Permanent Paralysis Of Limbs

✔️ Motor Neuron Disease With Permanent Symptoms

✔️ Multiple Sclerosis With Persisting Symptoms

✔️ Benign Brain Tumor

✔️ Blindness

✔️ Deafness

✔️ End Stage Lung Failure

✔️ End Stage Liver Failure

✔️ Loss Of Speech

✔️ Loss Of Limbs

✔️ Major Head Trauma

✔️ Primary (Idiopathic) Pulmonary Hypertension

✔️Third Degree Burns

ACKO Life Accidental Death Benefit Rider

ACKO Life Accidental Death Benefit Rider is one of the most affordable riders, purely designed to protect your family with an additional amount of money if your death is caused by an accident.

ACKO Life Accidental Total Permanent Disability Benefit Rider

Accidental Total Permanent Disability Rider is designed to protect your financial well-being in case a major accident leaves you permanently unable to work or care for yourself. It provides an extra amount to cover daily expenses. Additionally, we will waive off all future premiums of your ACKO Life Flexi Term Plan.

Why are Term Insurance Riders Important?

Term insurance riders are useful because they enhance your basic cover and give your family more financial security. Here are 4 key reasons why riders are important:

Increase Financial Protection: Riders increase the overall protection of your policy. For example, a critical illness rider provides a payout if you are diagnosed with a serious disease, while an accidental death rider gives extra coverage in case of an accident. These add-ons ensure your family gets more support beyond the basic life cover.

Affordable and Customisable: One of the main benefits of term insurance riders is that they are affordable. You can pick and choose riders based on your needs without having to buy a separate policy. This makes your plan customisable and flexible at a low cost.

Additional Tax Benefits: Adding riders to your term insurance plan may also give you extra tax savings. Premiums paid for certain riders, such as critical illness, can qualify for deductions under Section 80D of the Income Tax Act, in addition to the usual 80C benefits.

Peace of Mind: The biggest benefit of term insurance riders is peace of mind. Whether it’s illness, accident, or disability, these add-ons make sure your family is financially supported in tough times.

Eligibility Criteria To Buy a Term Insurance

To take a term insurance policy, you must fulfil certain eligibility criteria defined by the insurer. Knowing these criteria helps you select the appropriate plan.

Age Limit: The majority of insurers provide term plans to people aged between 18 and 65 years.

Income Criteria: Your income determines the maximum coverage amount you can choose.

Medical Fitness: Certain policies could ask for a medical test to evaluate your well-being.

Nationality & Residency: Applicable for Indians and NRIs according to insurance company guidelines.

Occupation & Lifestyle: Hazardous occupations or lifestyles like smoking could impact premium charges.

Note: Satisfying these conditions gives you a seamless approval process and brings you closer to ensuring your dear ones' future.

What is Covered and Not Covered in Term Insurance?

Term insurance gives financial help to your family. However, it’s important to know what it does and doesn’t cover. Always read the policy document to understand the full list.

What is Covered in Term Insurance:

What is Not Covered in Term Insurance:

Death Due to Illness

Death Due to Suicide in the First Year

Death Due to Accidents

Death from Risky Activities

Death Due to COVID-19 or Other Pandemic Diseases

Death from Criminal Acts

Death Due to Natural Causes

Death Due to pre-existing illnesses (undeclared)

Common Mistakes to Avoid When Buying Term Insurance

People make a lot of mistakes for various reasons when buying term insurance online. Here are some common mistakes you should avoid while buying term insurance in India:

Insufficient Calculation of Coverage Requirement: The biggest mistake is incorrectly calculating the coverage requirement. Factor in outstanding debts, future expenses such as children's education, and income replacement. If underestimated, this might result in less than adequate coverage for dependants.

Ignoring the Importance of Policy Duration: Choose the policy duration that coincides with your financial liabilities. In other words, if you have a mortgage of 20 years, you'd probably want your policy to last at least as long as the mortgage. Choosing insurance coverage until you’re 70 is a smart choice. Extending it beyond 70 can make your premiums (the amount you pay) much higher.

Not Considering Renewal Provisions: Most term insurance policies are renewable, but the premiums at renewal may be higher. Understand what the renewal provisions are, and how they compare to buying a new policy at a later date.

Not Comparing Quotes: Compare several quotes from different insurers to ensure that you get the best rate and terms for your needs.

Not Reading the Fine Print: Read the policy details carefully, and check the exclusions, limitations, and conditions that may apply to your coverage. You can also refer to theIRDAI’s Do’s and Don’ts for Life Insurance to understand what to look out for before buying a policy.

Not Accounting for Inflation: Consider how the value of your coverage may erode over time and additional coverage is needed to account for this.

Not Updating the Policy: Life circumstances change. Periodically review your policy and update it to determine whether it meets your needs.

Cheaper isn't Better: While the cost is an important factor in nearly anything, sometimes the cheapest policy isn't always the best. Make sure the insurer has a good reputation in terms of claim payouts and service to customers.

Not Researching the Insurer's Financial Health: Another mistake may be failing to research the insurance company's financial rating. An insurer that is financially stable is more likely to pay claims when they arise.

Not Knowing the Conversion Option: Many term policies have the option to convert to a permanent policy without a medical examination. This can be of great value if you believe that your needs might warrant permanent insurance protection in years to come.

Not Using Additional Riders: See if the policy offers additional riders, such as critical illness coverage or accidental death benefits that apply to you.

Why Should I Buy Term Life Insurance Online?

Buying a term plan online is quick, simple, and convenient. You can easily compare plans, choose what suits you best, and skip the paperwork. When you buy from ACKO, you get a smooth digital experience, transparent pricing, and helpful support. Here are some of the key benefits of buying your term insurance plan online:

Convenience: Buying term insurance online at ACKO is easy. You need not visit an office or meet an agent; you can complete the process anytime, anywhere, and at your own pace.

Cost-effective: Online term insurance plans at ACKO are pretty reasonably priced. With no middlemen or agents, you will be able to easily compare quotes from various providers and select the plan that fits your budget.

Transparency: Buying term insurance online from ACKO will show all the details and terms of the policy on our website. No hidden charges or confusing jargon-just straightforward information, pretty much like reading a book with no fine print.

Faster Process: There is no tedious paperwork and meetings. You can get the whole process done a lot faster at ACKO, sometimes in just a few minutes.

Multiple options at your fingertips: With ACKO, you have a wide variety of coverage options. In addition, you can customise your term insurance policy by choosing the coverage amount, policy term, and additional features like critical illness or accidental death benefit cover.

No Pressure: You may review every feature of the policy, understand its details, and eventually decide accordingly.

Secured Transactions: ACKO secures all your personal and financial information with advanced encryption and secure payment gateways. Your data is safe and secure.

How to Buy Term Insurance Online?

The process to buy the ACKO Life Flexi Term Plan is simple and straightforward. Follow the steps below:

Initiate the purchase journey via the widget on the website/app.

Select the plan

Answer the questions to determine eligibility and premium.

Pay the premium online.

Receive the policy via email or download it from the app.

Note: This is a generic process; the exact steps can vary depending on the chosen plan and other details.

Documents Required to Buy Term Insurance Plan

To buy a term insurance plan in India, you need a few simple documents. These help the company verify your details.

ID Proof

Aadhaar Card

Voter ID

PAN Card

Passport

Address Proof

Electricity, Telephone Bill etc (not more than 2 months old)

Aadhaar Card

Driving License

Age Proof

Birth Certificate

PAN Card (can be used again)

Income Proof

Salary Slip (for salaried people)

ITR (Income Tax Return) or bank statement (for self-employed)

Medical Reports (if asked)

Recent medical reports (health check-ups like blood test, blood pressure, etc)

Nominee KYC Documents

KYC documents of the nominee may be required. Some of these documents include Aadhaar Card, PAN Card, Passport, etc.

What are the Documents Required for Term Life Insurance Claim Process?

Death Certificate: This is the most crucial document. It proves that the person insured has passed away. You can get this from the local municipal authority or hospital where the person died.

Policy Document: You'll need a copy of the term life insurance policy. It shows the details of the insurance, like the coverage amount and beneficiary information.

Identification Proof: You'll need to prove who you are. Common forms of ID include a passport, Aadhaar card, or voter ID.

Medical Records: If the death was due to a medical reason, the insurance company might ask for medical documents or reports related to the illness or condition.

Police Report (if applicable): If the death happened under unusual or suspicious circumstances, you may need to provide a copy of the police report.

Nominee/Beneficiary ID: The person who will receive the insurance money (the nominee or beneficiary) must also prove their identity.

Bank Details: You must provide your bank account information where the insurance payout should be deposited. This is usually done through a cancelled cheque or a bank statement.

Proof of Relationship: If the nominee/beneficiary isn't the spouse, you may need proof of the relationship, like a marriage or birth certificate (for children).

Additional Documents: Depending on the specific circumstances of the claim, we might ask for more documents.

Why Customers Trust Our Term Insurance

Term insurance should give you peace of mind, knowing your family is protected. And getting covered should be just as easy.

We’ve made the buying process simple, quick, and transparent — with zero confusion.

4.6 / 5

Read what our customers have to say

Rated 4.6/5 with over 13632 reviews on Google

See all reviews

Terms Related To Term Insurance

Understanding these common terms will help you make better choices when buying a term insurance plan in India. Here is a list of some of the most important term plan terminologies.

Premiums: The regular amount agreed to paid (monthly, quarterly, half-yearly or annually) by the policyholder.

Maturity Benefit: Amount paid by the insurer when the policyholder outlives the policy term.

Death Benefit: Amount paid to the nominee if the policyholder passes away during the policy term.

Policy Term: Total duration of financial protection and benefits.

Insured Person/ Life Assured: Person covered under the policy.

Insurer: The policy provider that accepts the risk and pays for losses during the policy term.

Sum Assured/ Coverage: Amount the insurer pays during a claim.

Riders: Add-ons for extra protection, like Accidental Death or Critical Illness.

Grace Period: A window/time to pay premiums after the due date before the policy becomes inactive.

Lapse: Premiums are not paid, and the policy is not revived within the grace period, leading to a loss of coverage and no payout for beneficiaries. As per the Insurance Regulatory and Development Authority of India (IRDAI) guidelines, a term insurance policy that lapses due to non-payment of premiums generally loses coverage. The benefits can only be restored if the policy is revived within the permitted time as per policy terms.

Free Look Period: A window/time the insurer gives to the policyholder to review and cancel the policy without surrender charges.

Underwriting: The evaluation process insurers use to check your health, lifestyle, and other factors to determine your premium and application approval.

Find the Best Term Insurance Based on Your City

Choose term insurance smarter with city-specific insights on coverage, costs, and the protection your family truly needs.

A senior editor with years of expertise, she fine-tunes content that connects, converts, and builds trust. She transforms heavy life insurance concepts into clear, aha-moment reads. Writing is her passion, and thinking ahead is second nature. When not wrangling words, she’s crushing game levels because every challenge is a puzzle waiting to be solved.

Discover what the media is saying about ACKO Life Insurance

Our primary focus is to remain on protection biz, says ACKO Life's CEO Sandip Goenka

ACKO Life Insurance is doubling down on its protection focus, prioritising term insurance while also planning to expand into pensions and annuities, said the company's CEO Sandip Goenka, during an interaction with Moneycontrol. Read more

ACKO enters life insurance market with Flexi Term Life Insurance Plan

ACKO Tech, the parent company of ACKO General Insurance, has announced its expansion into the life insurance sector with the launch of ACKO Life Insurance. The company's debut offering is ACKO Flexi Term Life Insurance Plan. Read more

ACKO Tech launches life insurance plan: Read key features and details

ACKO Tech, the parent company of ACKO General Insurance, has launched ACKO Life Insurance with its new Flexi Term Life Insurance Plan. This move marks ACKO's expansion from general to life insurance. The ACKO Flexi Term Life Insurance Plan offers customizable coverage to adapt Read more

Disclaimer: The content on this page is generic and shared only for informational and explanatory purposes. It is based on industry experience and several secondary sources on the internet, and is subject to changes. Please go through the applicable policy wordings for updated ACKO-centric content, and before making any insurance-related decisions. For full disclaimer kindly click https://www.acko.com/life/disclaimer/