Protect your family with 100% pure life insurance

Coverage from

₹25 lakh to ₹100 crore

Adjust your coverage

when you need

ARN: L0130 | *T&C Apply

Coverage from

₹25 lakh to ₹100 crore

Adjust your coverage

when you need

Term insurance is the purest form of life insurance. It protects the people who depend on you. A term insurance plan gives your family a fixed amount of money if you pass away during the policy period. This money can help your dependents pay for food, clothing, healthcare, education, and other household expenses. That’s why choosing the best term insurance plan is important. It helps make sure your loved ones have long-term financial support in your absence.

Term insurance is the simplest form of life insurance that offers financial protection for a fixed number of years. It is an agreement between you and the insurance company. You pay a fixed amount regularly for a chosen period of time. If you pass away during those years, the insurance company gives a fixed amount of money to the person you have chosen (your nominee). A term insurance policy is a pure life insurance product. It does not pay any money at the end of the policy if you live through the full term. Its purpose is simple. It helps your family with money in case of your death.

For example, if a 25-year-old healthy non-smoker buys a ₹1 crore term insurance plan for 30 years, the premium can be quite affordable due to the person’s young age and good health. If he passes away during those 30 years, his nominee receives the full ₹1 crore. If he lives through the entire term, no money is paid at the end of the policy.

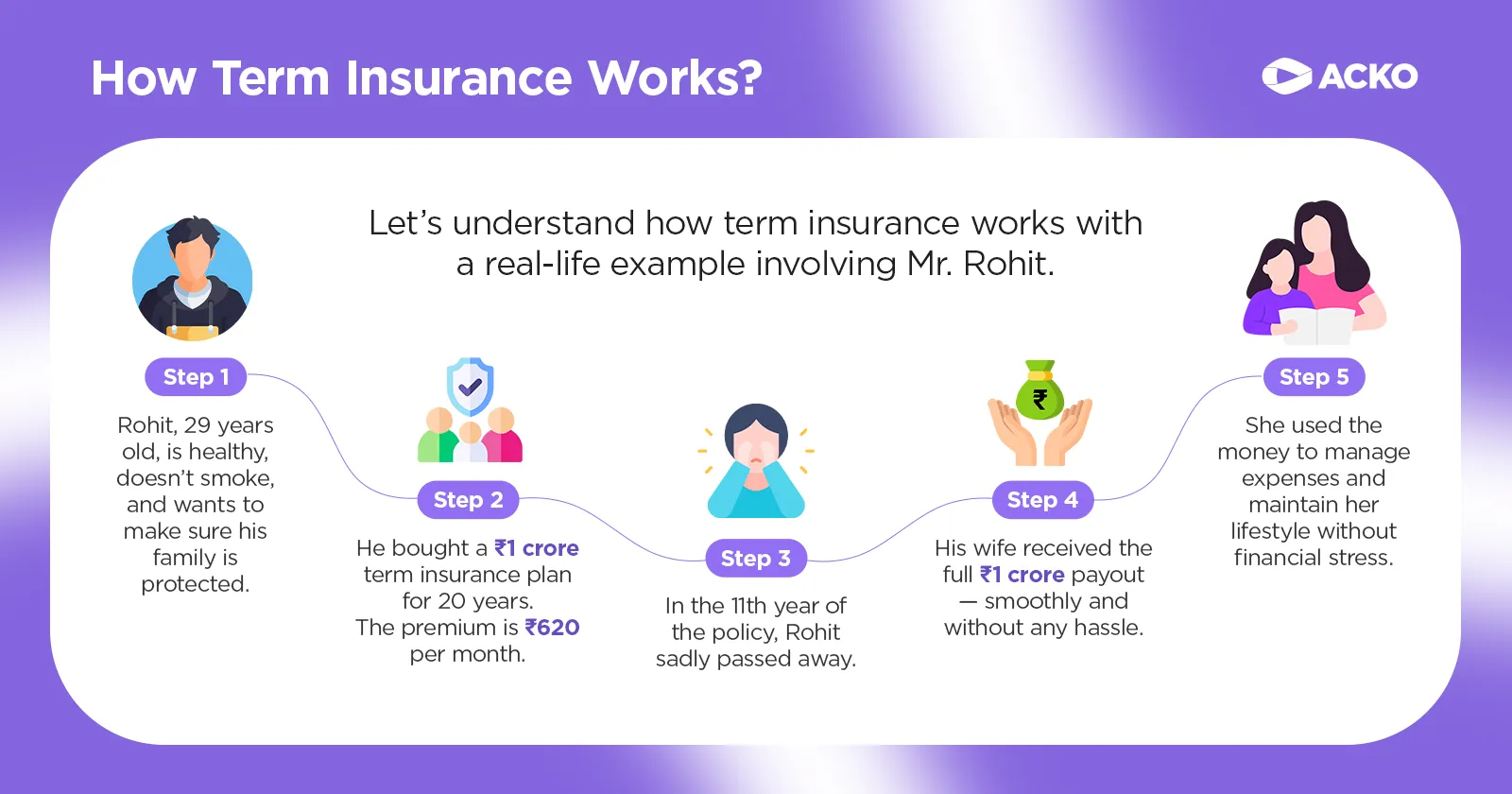

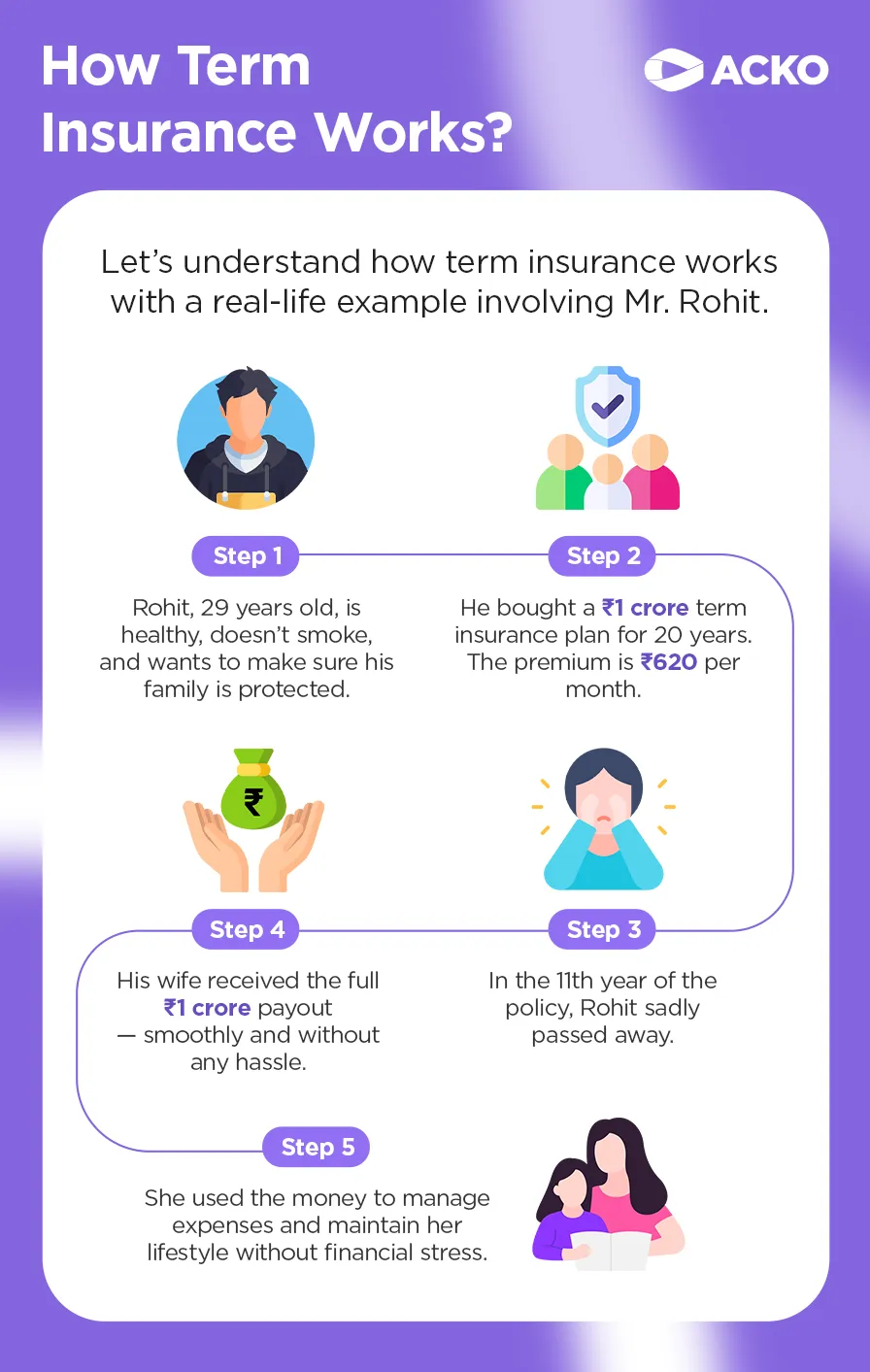

Let’s understand how term insurance works in the simplest way possible. All you need to do is follow these simple steps to see how a term plan protects your family:

You select a term insurance plan based on how much coverage your family would need and for how many years you want protection.

You pay a fixed premium (monthly or yearly) to keep the policy active for the chosen term.

As long as you continue paying the premium, your life is covered for the selected period.

If the insured person passes away during the policy term, the nominee (family member) receives the full sum assured.

The payout helps the family handle expenses like daily needs, loans, children’s education, and other financial responsibilities.

This is how term insurance works: simple, affordable protection to financially secure your family when they need it most.

The right time to buy a term insurance plan is as early as possible, because the earlier you buy, the cheaper it is and the longer your family stays protected. When you wait even 5-10 years to buy term insurance, your premium can increase by thousands, and you will have a shorter number of years of protection.

The image below explains how buying term insurance early can help reduce premiums.

A term insurance policy is a plan that helps take care of your family financially when you start taking on big life responsibilities. If something unexpected happens to you, it makes sure your loved ones have money to support their future plans and goals.

If you are the primary earner, term insurance provides financial security. For example, if you’re planning your children’s education and something unexpected happens, the policy payout can help continue their schooling without disruption.

Household costs like rent, bills, and daily living expenses continue regardless of circumstances. A term plan ensures these essentials are covered so your family can maintain their lifestyle.

If you have responsibilities such as a home loan, personal loan, or other liabilities, a term policy can help by providing funds to clear those obligations without burdening your family.

Term insurance works well with your long-term goals like retirement planning or wealth building. It gives you the confidence to invest in other areas, knowing your family’s basic financial security is covered.

If you contribute regularly to your household income, term insurance ensures your family still gets financial support. This can be especially helpful if your partner needs time to adjust career plans or childcare responsibilities.

Term insurance premiums and payouts are structured in a way that offers tax savings under applicable sections of the Income Tax Act, helping you plan your finances more efficiently.

Below is a simplified comparison of ACKO Pure Term Insurance vs Other Players’ Term Insurance to help you understand how ACKO stands out across key parameters that matter most to customers.

| Category | Details |

| Sum Assured | ₹25 lakh up to limits defined by the company’s underwriting policies. |

| Entry Age | 18 to 65 years |

| Policy Term | Flexible policy term options available |

| Premiums | Designed to be affordable for long-term life cover |

| Tax Benefits | Available as per applicable tax laws |

| Claim Settlement Ratio | 99.29% |

| Claim Process | Fully digital process with document upload. |

| Death Benefit | Available |

| Critical Illness Cover | Available |

| Accidental Death Benefit | Available |

| Accidental Total Permanent Disability Cover | Available |

| Claim Assistance | Dedicated support for claims |

| Customisable Coverage | Available |

Below is a simplified comparison of ACKO Pure Term Insurance vs Other Players’ Term Insurance to help you understand how ACKO stands out across key parameters that matter most to customers.

| Parameter | ACKO Pure Term Insurance | Other Players’ Term Insurance |

| Buying Process | 100% digital, paperless, quick online issuance | Often hybrid (agent + online), paperwork may be involved |

| Premium Pricing | Competitive pricing due to a digital-first model and lower overhead costs | Varies by insurer; some may have higher premiums due to distribution costs |

| Plan Structure | Pure protection-focused plan (no unnecessary bundled features) | Many plans include optional add-ons and bundled variants |

| Claim Process | Simple, digital-first claims experience | May involve offline documentation and longer processing |

| Transparency | Clear pricing and benefits are displayed upfront online | May require a detailed brochure review to understand exclusions |

| Medical Process | Simplified medical journey (as applicable) | May involve more extensive medical underwriting |

| Policy Management | Easy online access and self-service | Online access available, but may require agent support in some cases |

| Add-ons / Riders | Death rider options | A wide variety of riders, depending on the insurer |

| Speed of Issuance | Fast policy issuance (subject to underwriting) | Timelines vary across insurers |

ACKO Life Insurance is a fully IRDAI-licensed insurer focused on providing clear and dependable term insurance. A structured claims process and dedicated support help ensure families receive assistance when they need it most.

With ACKO Life, buying a term plan is simple, quick, and transparent — with zero confusion.

Term insurance gives financial help to your family. However, it’s important to know what it does and doesn’t cover. Always read the policy document to understand the full list.

| What is Covered in Term Insurance: | What is Not Covered in Term Insurance: |

| Death Due to Illness | Death Due to Suicide in the First Year |

| Death Due to Accidents | Death from Risky Activities |

| Death Due to COVID-19 or Other Pandemic Diseases | Death from Criminal Acts |

| Death Due to Natural Causes | Death Due to pre-existing illnesses (undeclared) |

The ideal coverage amount varies based on individual financial goals, liabilities, and family needs. A simple way to estimate this is to ensure the cover replaces your income and clears major financial responsibilities.

A commonly used rule is 15 - 20 times your annual income. For example, if you earn ₹10 lakh per year, a cover of ₹1 - 1.5 crore may help replace lost income for your family over the long term. Consider:

From this total, subtract:

In short, your term insurance cover should be adequate to help support your family’s lifestyle, repay debts, and fund important future goals comfortably.

In short, your term insurance cover should be adequate to help support your family’s lifestyle, repay debts, and fund important future goals comfortably.

Your term insurance needs evolve as your responsibilities grow. Here is an illustrative guide to help you understand how coverage may change at different life stages.

| Life Stage | Age Range | Typical Financial Obligations | Suggested Coverage Range | Illustrative Annual Premium Range* |

| Young Professional (Single) | 22–28 | Student loans, parents’ support | ₹50L – ₹1 Cr | ₹3,000 – ₹6,000 |

| Newly Married | 28–32 | Home loan planning, spouse protection | ₹1 – ₹1.5 Cr | ₹8,000 – ₹12,000 |

| New Parent | 30–35 | Home loan, child education | ₹1.5 – ₹2 Cr | ₹12,000 – ₹18,000 |

| Growing Family | 35–40 | Loans + education for two children | ₹2 – ₹3 Cr | ₹18,000 – ₹30,000 |

| Mid-Career | 40–45 | Remaining loans + college costs | ₹2 – ₹2.5 Cr | ₹25,000 – ₹40,000 |

| Pre-Retirement | 45–55 | Final obligations + spouse security | ₹1 – ₹2 Cr | ₹40,000 – ₹80,000 |

The cost of term insurance depends on a few basic factors, such as your age, the amount of life cover you choose, the policy term, and your health and lifestyle. Since term insurance focuses only on life protection, it is generally more affordable than other types of life insurance.

The easiest way to know how much your term insurance will cost is to calculate it based on your age, income, and coverage needs.

You can get ₹1 crore term insurance coverage starting at just ₹18/day*

You want to ensure your family's financial security in the event of your passing. However, you need to determine how much coverage you require or what the cost will be. That's where a Term Insurance Calculator comes in. In simple terms, a Term Insurance Calculator helps you determine how much insurance you need and how much it will cost. It's like a virtual assistant that takes the guesswork out of protecting your loved ones financially.

To take a term insurance policy, you must fulfil certain eligibility criteria defined by the insurer. Knowing these criteria helps you select the appropriate plan.

Note: Satisfying these conditions gives you a seamless approval process and brings you closer to ensuring your dear ones' future.

The process to buy a term insurance plan is simple. Follow the steps below:

Add details like your age, income, and lifestyle information to get an estimate.

Select the life cover amount and policy duration based on your needs. Use online premium calculators to get an estimate of the right coverage amount and premiums.

Answer health-related questions honestly. The medical tests required depend on your age and the coverage amount you're applying for. Some of the common term insurance medical tests include basic physical examination(height, weight, blood pressure), Blood tests, etc.

Once approved, complete the payment to activate your policy. Some of the common payment modes include Net banking, Debit/Credit card, UPI, and Digital wallets.

Tip: Pay annually to save compared to monthly payments

When you apply for a term insurance plan, the insurer will ask for a few basic documents to confirm who you are, understand your health and finances, and decide the right coverage for you. Below is a list of the key documents required:

| Document Type | Is It Mandatory? | Why It’s Needed? | When It’s Required? |

| Age Proof | Yes | To verify your age and calculate the correct premium | For all applications |

| Identity Proof | Yes | For KYC and identity verification | For all applications |

| Address Proof | Yes | For address verification and communication | For all applications |

| PAN Card | Yes | For tax compliance and income verification | Usually required for all policies |

| Income Proof | Yes | To confirm financial eligibility for higher coverage | When coverage exceeds ₹50 lakhs |

| Passport-size Photograph | Yes | For policy records and identity confirmation | For all applications |

| Medical Reports | Conditional | To assess health risks during underwriting | When coverage exceeds ₹50 lakhs or the age is above 40 |

| Bank Account Details | Yes | For premium payments, refunds, and claim payouts | For all applications |

| 3 Years ITR | Conditional | For financial underwriting | When coverage exceeds ₹1 crore |

| Net Worth Statement | Conditional | To justify very high coverage amounts | When coverage exceeds ₹5 crore |

This is how a claim settlement process for term life insurance works:

Note: Always keep copies of all submitted documents and maintain regular follow-up with the insurer’s claims team for updates.

Before you file a term insurance claim, you need to have a few important documents ready. Here is a list of documents required for a life insurance claim as per IRDAI.

You may be asked to submit extra documents depending on how the death occurred, such as a hospital record, police report, or post-mortem report. Some of the additional documents are listed below:

For natural death:

For accidental death:

For death abroad:

Understanding why claims get rejected helps you avoid these pitfalls:

| Rejection Reason | Prevention Strategy | Remedy if Rejected |

| Non-disclosure of medical history | Disclose all health conditions honestly | Usually none (claim denied) |

| Material misrepresentation | Provide accurate information in proposal | Very difficult to overturn |

| Policy lapsed (non-payment) | Set up auto-pay, pay within grace period | Revive policy within 2-5 years |

| Death during waiting period (suicide) | Only first 12 months exclusion | None - premiums returned |

| Death due to excluded causes | Read policy exclusions carefully | Depends on specific exclusion |

| Documentation incomplete/incorrect | Submit all original documents promptly | Resubmit with correct documents |

| Suspicious circumstances | Maintain transparent records | Investigation, possible legal action |

| Fraud/intentional concealment | Be completely honest | Claim denied + possible legal action |

Life insurance plans are designed for different needs. Understanding how term insurance compares with other life insurance options can help you choose a plan that matches your priorities and financial responsibilities.

At ACKO Life Insurance, the approach to life insurance is centred on clarity and a singular purpose: providing 100% pure protection without any added complexities. With that perspective, here’s how term insurance compares with other types of life insurance plans.

| Aspect | Term Insurance | Investment-Linked Life Insurance Plans |

| Primary purpose | Life protection | Protection combined with savings or investments |

| Premium cost | Lower | Higher |

| Returns | No returns | May offer returns based on market or policy performance |

| Life cover | Higher cover for the same premium | Lower cover for the same premium |

| Complexity | Simple and easy to understand | More complex structures |

| Focus | Financial security for the family | Long-term savings along with insurance |

| Example | 1 crore term insurance2 crore term insurance50 lakhs term insurance | ULIPs, endowment plans, and savings-linked life insurance |

Choosing the right term insurance plan in 2026 means balancing coverage, affordability, and flexibility. Here are the key factors to consider:

The first step is to figure out how much term insurance coverage you actually need. The coverage amount is also known as the sum assured (the money your family would receive if you pass away). So, it’s one of the most important decisions because it directly affects your family’s financial security and also your policy premium.

You can maximise your coverage by adding suitable riders, such as accidental death benefits, permanent disability cover, or daily hospital cash, to ensure broader financial protection during unforeseen travel emergencies.

The next thing you’ll want to do is choose how long you want your term insurance coverage to last. The policy term means how many years your plan will provide protection, and there are some simple ways to decide this:

Now that you have determined your term insurance coverage and policy term, your next step is to choose your premium payment option. The premium payment option can impact your budget, payment convenience, and long-term financial planning; thus, it is best to choose a premium payment option that you are comfortable with. You can choose either:

1. Regular Pay:

2. Limited Pay (10-15 years):

When you buy a term insurance plan, you’ll need to go through a quick medical check-up. This step is called medical underwriting. This is an important step of the process because it ensures your premiums are based on your actual health conditions.

Once your application and medical underwriting are done, your term insurance policy is issued. This is when your coverage officially starts, and you will receive your policy document (digitally or physically) with all the details about your plan.

Understanding these common terms will help you make better choices when buying a term insurance plan in India. Here is a list of some of the most important term plan terminologies.

The regular amount agreed to be paid (monthly, quarterly, half-yearly or annually) by the policyholder.

Amount paid by the insurer when the policyholder outlives the policy term.

Amount paid to the nominee if the policyholder passes away during the policy term

Total duration of financial protection and benefits.

Person covered under the policy.

The policy provider that accepts the risk and pays for losses during the policy term.

Amount the insurer pays during a claim.

Add-ons for extra protection, like Accidental Death or Critical Illness.

A window/time to pay premiums after the due date before the policy becomes inactive.

A window/time the insurer gives to the policyholder to review and cancel the policy without surrender charges.

Premiums are not paid, and the policy is not revived within the grace period, leading to a loss of coverage and no payout for beneficiaries. As per the Insurance Regulatory and Development Authority of India (IRDAI) guidelines, a term insurance policy that lapses due to non-payment of premiums generally loses coverage. The benefits can only be restored if the policy is revived within the permitted time as per policy terms.

The evaluation process insurers use to check your health, lifestyle, and other factors to determine your premium and application approval.

Before you buy term insurance, it’s natural to have many questions. It’s an important product that takes time to finalise, so you want to be sure about your choices. Here are some answers to common questions people have about term insurance in India.

![]()

ACKO Life Insurance is doubling down on its protection focus, prioritising term insurance while also planning to expand into pensions and annuities, said the company's CEO Sandip Goenka, during an interaction with Moneycontrol. Read more

ACKO Tech, the parent company of ACKO General Insurance, has announced its expansion into the life insurance sector with the launch of ACKO Life Insurance. The company's debut offering is ACKO Flexi Term Life Insurance Plan. Read more

ACKO Tech, the parent company of ACKO General Insurance, has launched ACKO Life Insurance with its new Flexi Term Life Insurance Plan. This move marks ACKO's expansion from general to life insurance. The ACKO Flexi Term Life Insurance Plan offers customizable coverage to adapt Read more

Disclaimer: The content on this page is generic and shared only for informational and explanatory purposes. It is based on industry experience and several secondary sources on the internet, and is subject to changes. Please go through the applicable policy wordings for updated ACKO-centric content, and before making any insurance-related decisions. For full disclaimer kindly click https://www.acko.com/life/disclaimer/

Written by

Neviya Laishram

Senior Editor

A senior editor with years of expertise, she fine-tunes content that connects, converts, and builds trust. She transforms heavy insurance concepts into clear, aha-moment reads. Writing is her passion, and thinking ahead is second nature. When not wrangling words, she’s crushing game levels because every challenge is a puzzle waiting to be solved.

Reviewed by

Vaibhav Kumar Kaushik

Senior Director – Life Insurance Strategy

Senior Director – Life Insurance Strategy at Acko, I drive customer-centric, digitally led strategies that shape the future of Life insurance. With expertise in new business development, D2C growth, and investment management, I’ve helped build and scale Acko’s Term Life offerings by aligning customer insights with innovative product strategy to fuel sustainable growth.

#36/5, Hustlehub One East, Somasandrapalya 27th Main Rd, Sector 2, HSR Layout, Bengaluru, Karnataka 560102